If you're considering purchasing a home and are affiliated with Navy Federal Credit Union, you might be wondering, Can I get a mortgage with Navy Federal? The answer is yes—Navy Federal offers a variety of mortgage options tailored to meet the needs of military members, veterans, and their families. With competitive interest rates, flexible terms, and specialized programs like VA loans, Navy Federal provides accessible and affordable home financing solutions. Whether you're a first-time homebuyer or looking to refinance, their dedicated team and member-focused approach make the mortgage process smoother and more supportive. To qualify, you’ll need to meet their eligibility criteria, which typically include membership in the credit union and a solid credit history. Exploring their mortgage offerings can be a smart step toward achieving your homeownership goals.

Explore related products

What You'll Learn

![]()

Credit Score Requirements

Navy Federal Credit Union, like most lenders, evaluates your creditworthiness through your credit score, a numerical representation of your financial history. This three-digit number, typically ranging from 300 to 850, holds significant weight in determining your eligibility for a mortgage and the terms you'll receive.

Navy Federal doesn't publicly disclose a strict minimum credit score requirement for mortgages, opting instead for a more holistic approach. This means they consider your entire financial profile, including income, debt-to-income ratio, and employment history, alongside your credit score. However, understanding the general credit score landscape for mortgages is crucial.

Understanding the Credit Score Spectrum:

While Navy Federal's flexibility is encouraging, it's helpful to understand the typical credit score ranges and their implications for mortgage approval. Generally, scores above 740 are considered excellent, often qualifying borrowers for the most favorable interest rates and terms. Scores between 670 and 739 are deemed good, still offering access to competitive rates but with potentially slightly higher interest. Scores below 670 may present challenges, with lenders potentially requiring larger down payments or offering less favorable terms. Scores below 620 are often considered subprime, making mortgage approval more difficult and potentially requiring specialized lenders.

Remember, these are general guidelines, and Navy Federal's individualized approach means they may consider applicants with scores outside these ranges based on their overall financial picture.

Boosting Your Credit Score for Mortgage Success:

If your credit score isn't where you'd like it to be, don't despair. Several strategies can help you improve it before applying for a Navy Federal mortgage. Paying bills on time, every time, is paramount. Late payments can significantly damage your score. Aim to keep credit card balances below 30% of their limits, as high credit utilization can negatively impact your score. Regularly reviewing your credit report for inaccuracies and disputing any errors is crucial. Consider using a credit monitoring service to track your progress and identify areas for improvement.

Building a positive credit history takes time, so start implementing these strategies well in advance of your mortgage application.

Navy Federal's Commitment to Serving Its Members:

Navy Federal's mission to serve its members, including active duty military, veterans, and their families, extends to its mortgage lending practices. They understand the unique financial challenges faced by military personnel and offer specialized programs and resources to support their homeownership goals. This commitment often translates into more flexible lending criteria and personalized guidance throughout the mortgage process.

Navy Federal's dedication to its members means they are more likely to work with borrowers who may not meet traditional credit score thresholds but demonstrate strong financial responsibility and a commitment to homeownership.

Steps to Open a Navy Federal Account: Requirements and Tips

You may want to see also

Explore related products

![]()

Loan Types Offered

Navy Federal Credit Union offers a diverse range of mortgage loan types tailored to meet the unique needs of its members, particularly those with military affiliations. Among the most popular options is the VA Loan, which requires no down payment and is backed by the Department of Veterans Affairs. This loan is ideal for active-duty service members, veterans, and their spouses, offering competitive interest rates and no private mortgage insurance (PMI) requirement. For those who don’t qualify for a VA Loan, Navy Federal provides conventional loans, which typically require a down payment of at least 3% to 20%, depending on the borrower’s creditworthiness. These loans are versatile and can be used for primary residences, second homes, or investment properties.

Another standout option is the FHA Loan, insured by the Federal Housing Administration, which is designed for first-time homebuyers or those with lower credit scores. With a minimum down payment of 3.5%, this loan is more accessible but comes with mortgage insurance premiums. Navy Federal also offers adjustable-rate mortgages (ARMs), which start with a fixed interest rate for an initial period (e.g., 5, 7, or 10 years) before adjusting annually based on market conditions. ARMs can be advantageous for borrowers who plan to sell or refinance before the rate adjusts.

For members looking to build or renovate, Navy Federal provides construction loans, which cover the cost of land purchase and home construction, converting to a permanent mortgage once the project is complete. Additionally, jumbo loans are available for properties exceeding conforming loan limits, typically starting at $726,200 in most areas. These loans cater to high-value homes but may require larger down payments and stricter credit qualifications.

Choosing the right loan type depends on factors like financial stability, long-term plans, and eligibility. Navy Federal’s loan officers work closely with members to assess their situations and recommend the best fit. For instance, a young military family might benefit from a VA Loan’s flexibility, while a seasoned homeowner refinancing a high-value property could opt for a jumbo loan. Understanding these options ensures borrowers make informed decisions aligned with their goals.

Lastly, Navy Federal’s HomeBuyers Choice Mortgage is worth noting, as it offers 100% financing for primary residences, eliminating the need for a down payment. While it requires funding fees and mortgage insurance, it’s a viable alternative for those without VA eligibility. Each loan type comes with its own set of advantages and considerations, making it essential to evaluate personal circumstances before committing. Navy Federal’s commitment to serving military members and their families is evident in its comprehensive loan portfolio, designed to simplify the path to homeownership.

Navy Reserves Benefits: Can You Get College Paid While Serving?

You may want to see also

Explore related products

![]()

Down Payment Options

Navy Federal Credit Union offers a variety of mortgage options, and understanding your down payment choices is crucial to securing the right loan for your financial situation. One of the most appealing aspects of Navy Federal’s mortgage programs is the flexibility in down payment requirements, which can significantly reduce upfront costs for borrowers. For instance, their 100% financing options, such as the HomeBuyers Choice program, eliminate the need for a down payment entirely, making homeownership more accessible for military members and their families. This program also waives private mortgage insurance (PMI), further reducing monthly expenses.

For those who prefer to make a down payment, Navy Federal allows as little as 3% down on conventional loans, a lower threshold than many traditional lenders. This option is particularly beneficial for first-time homebuyers who may not have substantial savings. However, it’s important to note that a smaller down payment often results in higher monthly payments and may require PMI, which adds to the overall cost of the loan. Borrowers should weigh these factors against their long-term financial goals.

Another down payment option is the use of gift funds, which Navy Federal permits for certain loan types. Family members or eligible organizations can contribute to your down payment, easing the financial burden. For example, if your parents wish to help you purchase a home, their gift can be applied directly to your down payment, provided proper documentation is submitted. This flexibility can be a game-changer for borrowers with limited personal savings.

Lastly, Navy Federal encourages borrowers to explore government-backed loans, such as VA loans, which offer 100% financing and are exclusive to eligible military personnel, veterans, and their spouses. These loans not only eliminate the down payment requirement but also come with competitive interest rates and no PMI. For those who qualify, VA loans are often the most cost-effective option available. By carefully evaluating these down payment options, borrowers can choose the path that best aligns with their financial capabilities and homeownership aspirations.

Navy SEALs to Admirals: Uncommon Promotions in Naval Leadership

You may want to see also

Explore related products

![]()

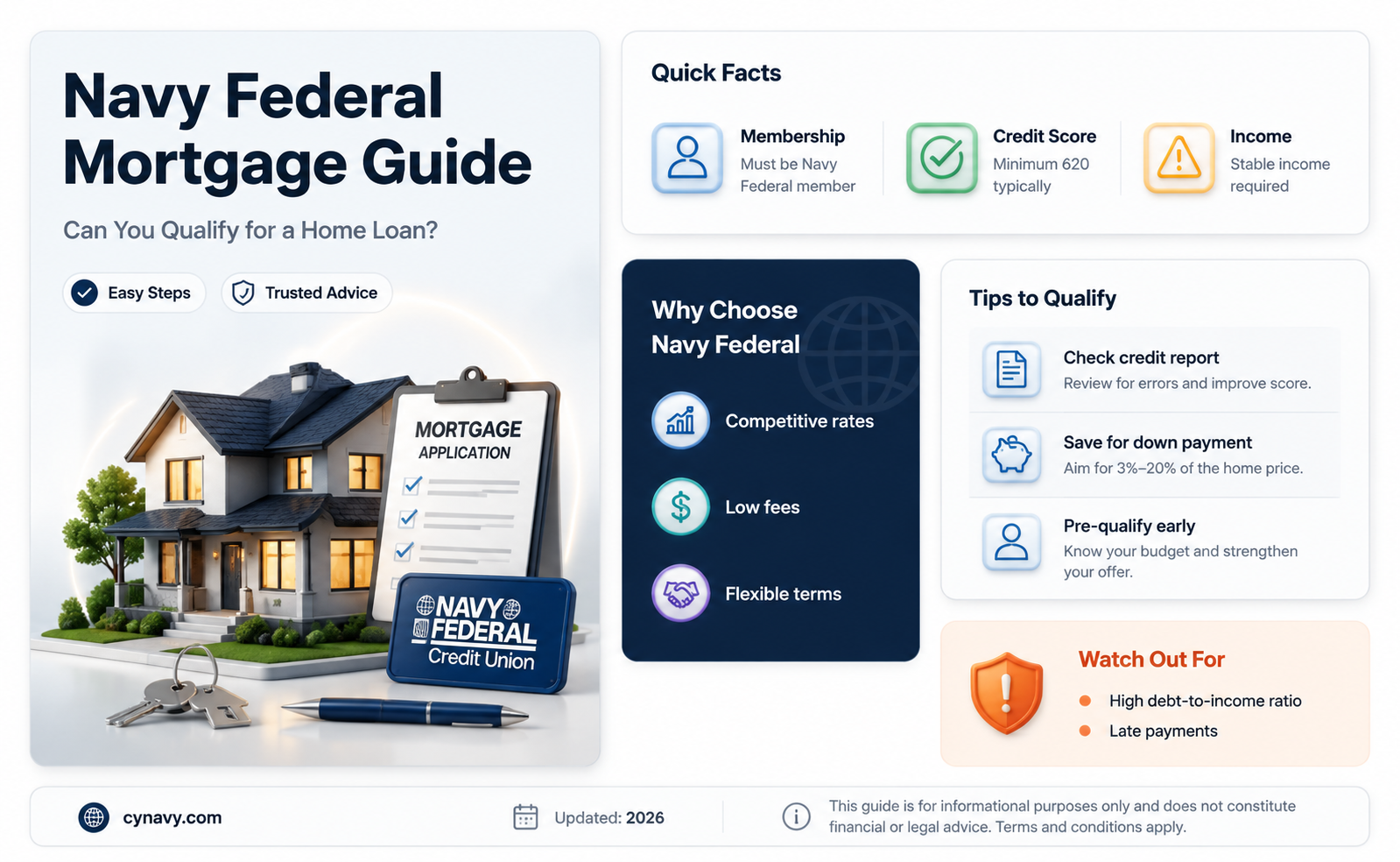

Eligibility Criteria

Navy Federal Credit Union offers mortgages tailored to its members, but not everyone qualifies. Membership itself is the first hurdle: you must be an active-duty or retired military member, a veteran, a Department of Defense civilian employee, or a family member of someone who fits these categories. Without this affiliation, your mortgage journey with Navy Federal ends before it begins.

Beyond membership, creditworthiness plays a pivotal role. Navy Federal typically looks for a minimum credit score of 620 for conventional loans, though higher scores unlock better rates and terms. For VA loans, which are a specialty, the credit requirements can be more flexible, sometimes accepting scores as low as 600. However, a lower score often means stricter scrutiny of your financial history, including debt-to-income ratio (DTI), which should ideally be below 41%.

Income stability is another critical factor. Lenders want assurance that you can repay the loan, so consistent employment and a steady income stream are essential. Self-employed borrowers face additional scrutiny, often needing two years of tax returns to demonstrate reliability. If you’ve recently changed jobs, be prepared to explain how your new role maintains or improves your financial stability.

Finally, your down payment and savings matter. While Navy Federal offers 100% financing options like VA loans, conventional loans typically require at least 3% down. A larger down payment not only reduces your loan amount but also signals financial discipline, potentially lowering your interest rate. Additionally, having reserves—savings equivalent to 2–6 months of mortgage payments—can strengthen your application, showing you’re prepared for unexpected expenses.

In summary, eligibility for a Navy Federal mortgage hinges on membership, credit health, income stability, and financial preparedness. Each criterion serves as a piece of the puzzle, and addressing them proactively increases your chances of approval. Whether you’re a first-time homebuyer or a seasoned investor, understanding these requirements is the first step toward securing your dream home with Navy Federal.

Your Guide to Joining the Navy: Steps, Requirements, and Tips

You may want to see also

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/61U70FDHeVL._AC_UL320_.jpg)

![]()

Interest Rates & Terms

Navy Federal Credit Union offers a range of mortgage options with competitive interest rates, but understanding the nuances can significantly impact your long-term financial health. Fixed-rate mortgages, for instance, lock in your interest rate for the life of the loan, providing stability and predictability. For example, as of recent data, Navy Federal’s 30-year fixed-rate mortgage might hover around 6.5%, while a 15-year term could be closer to 5.75%. These rates are subject to market fluctuations, so timing your application during a rate dip can save thousands over the loan’s lifespan.

Adjustable-rate mortgages (ARMs) from Navy Federal start with a lower introductory rate, typically fixed for 5, 7, or 10 years, before adjusting annually. While this can be appealing for short-term savings, it’s crucial to assess your financial outlook. If you plan to sell or refinance before the adjustment period ends, an ARM could be advantageous. However, if you stay long-term, prepare for potential rate increases tied to market indices like the LIBOR or SOFR. Navy Federal caps rate adjustments to protect borrowers, but understanding these limits is essential.

Loan terms also play a pivotal role in your mortgage decision. Shorter terms, like 15 years, come with higher monthly payments but lower overall interest costs. For instance, a $250,000 mortgage at 5.75% over 15 years would save approximately $100,000 in interest compared to a 30-year term. Conversely, longer terms reduce monthly payments, freeing up cash flow for other financial goals. Navy Federal’s calculators can help you model these scenarios to find the right balance for your budget.

Eligibility for Navy Federal’s best rates often depends on your credit score, debt-to-income ratio, and down payment. A credit score of 740 or higher typically secures the most favorable terms, while lower scores may result in slightly higher rates. Additionally, Navy Federal offers VA loans with no down payment requirement and no private mortgage insurance (PMI), which can lower upfront and monthly costs for eligible service members and veterans.

Finally, consider Navy Federal’s unique benefits, such as no origination fees on certain loans and personalized service tailored to military families. These perks can offset slightly higher rates if they exist, making it a holistic choice rather than a purely rate-driven decision. Always compare Navy Federal’s offerings with other lenders, but factor in the added value of membership benefits and specialized support.

Joining Navy Federal: Eligibility, Application, and Membership Benefits Explained

You may want to see also

Frequently asked questions

Yes, Navy Federal offers mortgages to active-duty military, veterans, retirees, and their families, as well as civilians who meet their eligibility requirements.

To be eligible, you must be a Navy Federal Credit Union member. Membership is open to active-duty military, veterans, retirees, and their families, as well as Department of Defense civilians and contractors.

Yes, Navy Federal offers VA loans, which provide benefits such as no down payment requirement, no private mortgage insurance (PMI), and competitive interest rates for eligible veterans, active-duty service members, and their spouses.

Navy Federal offers a variety of mortgage options, including fixed-rate mortgages, adjustable-rate mortgages (ARMs), VA loans, FHA loans, and jumbo loans, tailored to meet different financial needs and preferences.

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)