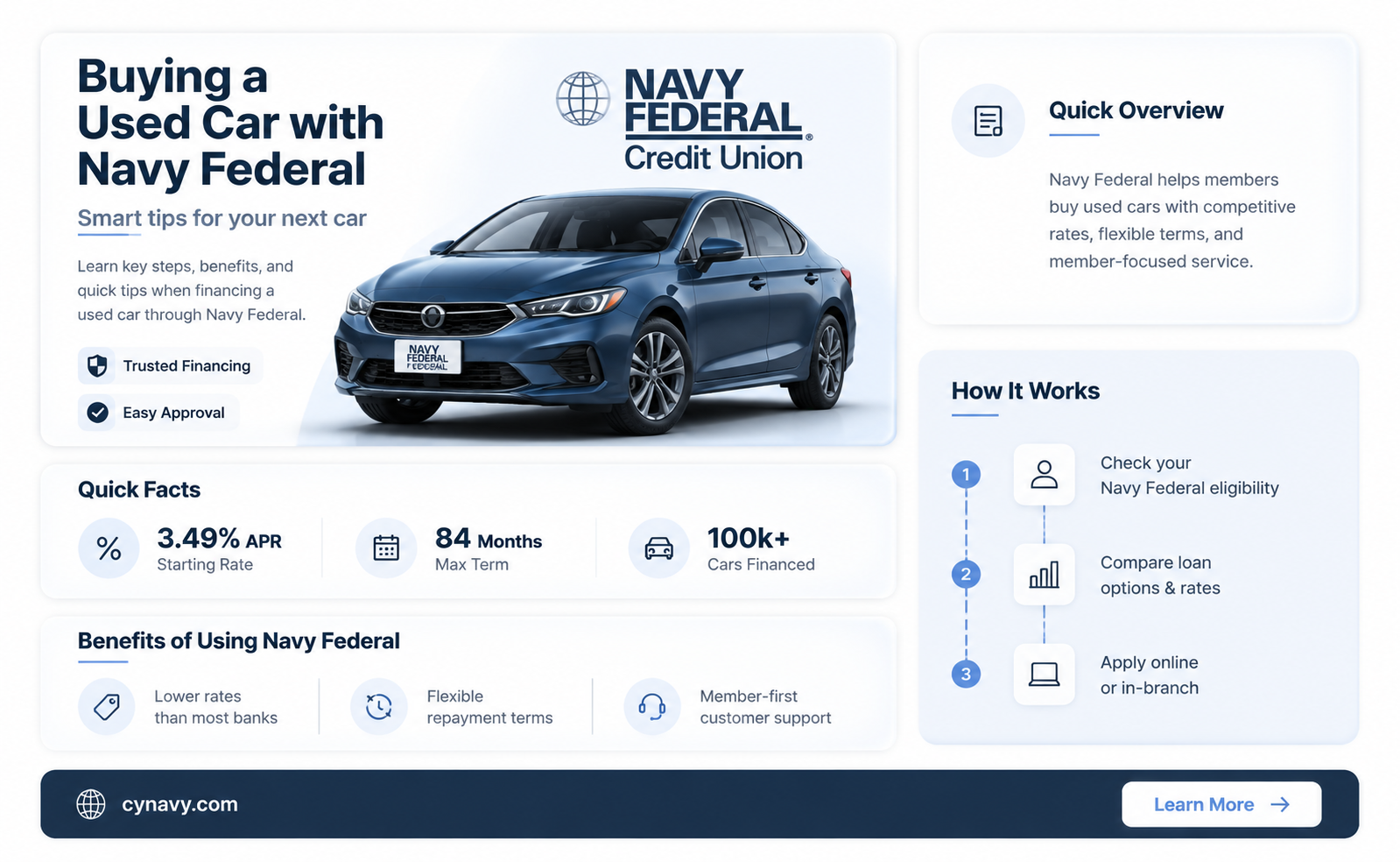

If you're considering purchasing a used car and are a member of Navy Federal Credit Union, you might be wondering if you can secure financing through them. Navy Federal offers a range of auto loan options, including those for used vehicles, which can provide competitive rates and flexible terms tailored to your financial situation. Whether you're a military member, veteran, or family member, Navy Federal’s auto loans often come with benefits like no application fees, potential discounts, and the convenience of working with a trusted financial institution. Before applying, it’s a good idea to check your eligibility, review their loan requirements, and compare rates to ensure you’re getting the best deal for your used car purchase.

| Characteristics | Values |

|---|---|

| Eligibility | Navy Federal members, including active duty, retired military, veterans, and their families |

| Loan Types | New and used auto loans, private party auto loans, auto loan refinancing |

| Loan Terms | Up to 96 months (8 years) for new and used cars |

| Loan Amounts | Up to 120% of the vehicle's value (including tax, title, and license) |

| Interest Rates | As low as 1.74% APR (Annual Percentage Rate) for well-qualified borrowers (rates as of October 2023) |

| Down Payment | No minimum down payment required, but a larger down payment can lower the interest rate and monthly payments |

| Vehicle Age | Up to 15 years old for used cars |

| Mileage Limit | Up to 120,000 miles for used cars |

| Application Process | Online, by phone, or in-person at a Navy Federal branch |

| Approval Time | As fast as 24 hours, depending on the application and vehicle information |

| Additional Benefits | No application or prepayment fees, potential discounts for automatic payments, and access to Navy Federal's car-buying service |

| Credit Requirements | Good to excellent credit (typically 680+ credit score) for the best rates, but borrowers with lower credit scores may still qualify |

| Loan Servicing | Navy Federal services its own loans, providing a single point of contact for borrowers |

| GAP Insurance | Available for purchase to cover the difference between the loan balance and the vehicle's value in case of total loss |

| Mechanical Repair Coverage | Available for purchase to cover repairs after the manufacturer's warranty expires |

| Latest Update | Information accurate as of October 2023; rates and terms subject to change |

Explore related products

What You'll Learn

- Eligibility Requirements: Check Navy Federal’s criteria for used car loans, including credit score and membership

- Loan Rates: Compare Navy Federal’s used car loan interest rates with other lenders

- Loan Limits: Understand maximum loan amounts for used cars through Navy Federal

- Application Process: Steps to apply for a used car loan with Navy Federal

- Additional Benefits: Explore perks like loan discounts or payment flexibility for members

![]()

Eligibility Requirements: Check Navy Federal’s criteria for used car loans, including credit score and membership

To secure a used car loan through Navy Federal Credit Union, understanding their eligibility criteria is paramount. Membership is the first hurdle: you must be an active-duty or retired military member, a veteran, a Department of Defense civilian employee, or a family member of someone who fits these categories. Without this affiliation, Navy Federal’s services, including auto loans, are off-limits. Think of membership as the key that unlocks access to their competitive rates and terms.

Once membership is confirmed, your credit score becomes the next critical factor. Navy Federal typically looks for a minimum credit score of 600 for auto loans, though higher scores (700 and above) can secure more favorable interest rates. If your score falls below 600, you may still qualify but expect higher rates or the need for a co-signer. It’s worth noting that Navy Federal evaluates your overall financial health, including debt-to-income ratio and credit history, so a strong credit profile beyond just the score can work in your favor.

Income stability is another cornerstone of eligibility. Navy Federal requires proof of consistent income to ensure you can repay the loan. This doesn’t necessarily mean a high salary, but rather a reliable source of funds, such as a steady job or retirement benefits. If you’re self-employed or have irregular income, additional documentation, like tax returns or bank statements, may be required to demonstrate financial stability.

Finally, the age and condition of the used car you’re financing can impact eligibility. Navy Federal typically finances vehicles up to 15 years old, though newer models may qualify for better terms. The car’s value, as determined by Kelley Blue Book or a similar appraisal tool, must also align with the loan amount requested. If the car’s value is significantly lower than the loan, you may need to adjust your budget or consider a smaller loan.

In summary, Navy Federal’s used car loan eligibility hinges on membership, creditworthiness, income stability, and the vehicle’s specifics. By meeting these criteria, you position yourself to take advantage of their competitive rates and flexible terms. Always review their latest requirements, as criteria can evolve, and consider pre-approval to streamline the car-buying process.

Joining the Navy SEALs: Essential Steps to Achieve Your Elite Dream

You may want to see also

Explore related products

![]()

Loan Rates: Compare Navy Federal’s used car loan interest rates with other lenders

Navy Federal Credit Union offers competitive used car loan rates, but how do they stack up against other lenders? A side-by-side comparison reveals key differences that can save you money. For instance, as of 2023, Navy Federal’s starting APR for used car loans is 4.29% for terms up to 36 months, while traditional banks like Bank of America offer rates starting at 4.49% for similar terms. Credit unions like PenFed, another military-focused institution, start at 4.44%. Online lenders like LightStream, known for their low rates, begin at 5.49% but may offer higher limits. This snapshot shows Navy Federal’s slight edge, but rates fluctuate based on credit score, loan term, and vehicle age. Always check current rates and consider your eligibility for Navy Federal’s membership-based benefits.

To compare effectively, start by identifying your credit score, as it’s the primary driver of your interest rate. Navy Federal often provides lower rates for borrowers with scores above 700, while other lenders may penalize scores below 680 more severely. For example, a borrower with a 720 score might secure a 4.5% rate at Navy Federal, compared to 5.2% at a regional bank. Use online calculators to estimate monthly payments and total interest costs for different lenders. Pro tip: Navy Federal’s rate discounts for automatic payments and relationship pricing can further narrow the gap, making their rates even more attractive for eligible members.

Another critical factor is loan term flexibility. Navy Federal offers terms up to 84 months for used cars, but longer terms often come with higher rates. For instance, a 72-month loan might have a 5.99% APR, while a 36-month loan stays at 4.29%. Compare this to banks like Chase, which caps used car loans at 72 months with rates starting at 5.74%. If you prioritize lower monthly payments, Navy Federal’s longer terms could be beneficial, but you’ll pay more in interest over time. Shorter terms save money but require higher monthly payments—choose based on your budget and financial goals.

Beyond rates, consider lender-specific perks. Navy Federal waives fees for used car loans and offers pre-approvals valid for 60 days, giving you bargaining power at dealerships. In contrast, online lenders like LendingClub may charge origination fees of up to 8%, eating into your savings. Some banks provide rate discounts for existing customers, but Navy Federal’s military-focused benefits, like deferred payments during active duty, are unique. Weigh these extras against rate differences to determine the best overall value for your situation.

Finally, eligibility matters. Navy Federal restricts membership to military personnel, veterans, and their families, so not everyone can access their rates. If you’re ineligible, explore credit unions with broader membership criteria or compare national banks and online lenders. For example, Alliant Credit Union offers used car rates starting at 4.35% with no military affiliation required. While Navy Federal’s rates are competitive, ensure you qualify before ruling out other options. Always read the fine print, as some lenders exclude older vehicles or impose mileage limits that could affect your loan approval.

Earning a College Degree While Serving in the Navy: Is It Possible?

You may want to see also

Explore related products

![]()

Loan Limits: Understand maximum loan amounts for used cars through Navy Federal

Navy Federal Credit Union offers used car loans with specific maximum limits, ensuring members can finance their purchases responsibly. Understanding these limits is crucial for budgeting and setting realistic expectations. For instance, as of recent data, Navy Federal caps used car loans at $50,000 for vehicles up to 5 years old, while older models may have lower limits. This structure reflects the depreciation of vehicles over time and helps mitigate risk for both the lender and borrower.

Analyzing these loan limits reveals a strategic approach to financing. Navy Federal considers factors like vehicle age, mileage, and condition to determine the maximum loan amount. For example, a 3-year-old sedan in excellent condition might qualify for the full $50,000, whereas a 7-year-old SUV with higher mileage could be limited to $30,000. This tiered system encourages members to invest in well-maintained vehicles while avoiding overextension on older, less reliable cars.

To navigate these limits effectively, follow these steps: first, research the value of the used car you’re interested in using tools like Kelley Blue Book. Next, compare this value to Navy Federal’s loan limits for the vehicle’s age category. Finally, factor in additional costs like taxes, registration, and warranty fees, as these are often included in the loan amount. Pro tip: Aim for a down payment of at least 10–20% to reduce the loan amount and improve your chances of approval.

A cautionary note: exceeding Navy Federal’s loan limits can lead to higher interest rates or outright denial. For instance, attempting to finance a $60,000 used luxury car may result in a loan offer capped at $50,000, leaving you to cover the difference. Additionally, older vehicles with high mileage may not qualify for financing at all, as they pose greater risk. Always verify eligibility before committing to a purchase.

In conclusion, Navy Federal’s used car loan limits are designed to balance accessibility with financial prudence. By understanding these caps and planning accordingly, members can secure financing that aligns with their needs and budget. Whether you’re eyeing a late-model compact or a mid-range SUV, knowing the limits ensures a smoother loan process and a smarter purchase decision.

Can Army and Navy Athletes Enter the NFL Draft?

You may want to see also

![]()

Application Process: Steps to apply for a used car loan with Navy Federal

Securing a used car loan with Navy Federal Credit Union is a straightforward process designed to cater to the financial needs of military members, veterans, and their families. The application process is streamlined to ensure efficiency, but it requires careful preparation to maximize your chances of approval. Here’s a step-by-step guide to navigating the application process effectively.

Step 1: Verify Eligibility and Membership

Before applying, confirm your eligibility for Navy Federal membership. This typically includes active-duty military, veterans, retirees, and their families. If you’re not already a member, you’ll need to join the credit union. Membership is a prerequisite for accessing their loan products, including used car financing. Navy Federal’s website offers a quick eligibility checker to simplify this step.

Step 2: Gather Required Documentation

Preparation is key to a smooth application. You’ll need proof of identity (e.g., driver’s license), income verification (recent pay stubs or tax returns), and details about the used car you intend to purchase, such as the VIN, make, model, and year. If you’re trading in a vehicle, have its information ready as well. Organizing these documents beforehand can expedite the process and reduce delays.

Step 3: Complete the Application

Navy Federal offers multiple application channels: online, over the phone, or in person at a branch. The online application is the most convenient, allowing you to input your personal, financial, and vehicle details at your own pace. Be accurate and thorough, as incomplete or incorrect information can lead to delays or rejection. If you’re unsure about any section, Navy Federal’s customer service team is available to assist.

Step 4: Review Loan Terms and Rates

Once your application is submitted, Navy Federal will assess your creditworthiness and provide loan offers tailored to your profile. Pay close attention to the interest rate, loan term, and monthly payment amount. Navy Federal often offers competitive rates for used car loans, but it’s wise to compare these terms with other lenders to ensure you’re getting the best deal. Consider using their loan calculator to estimate costs before finalizing.

Step 5: Finalize and Fund the Loan

After selecting your preferred loan terms, finalize the agreement. Navy Federal will disburse the funds directly to the dealership or seller, simplifying the purchase process. Ensure all paperwork is signed and submitted promptly to avoid any holdups. Once the loan is funded, you’ll begin making payments according to the agreed schedule.

Cautions and Tips

While Navy Federal’s application process is user-friendly, there are a few pitfalls to avoid. First, don’t apply without checking your credit score, as a low score may affect your eligibility or interest rate. Second, be realistic about your budget—borrowing more than you can afford can lead to financial strain. Lastly, read the fine print to understand any fees or penalties associated with the loan.

In conclusion, applying for a used car loan with Navy Federal is a structured process that rewards preparation and attention to detail. By following these steps and staying informed, you can secure financing that aligns with your financial goals and lifestyle.

Did Pete Hegseth Get Fired? Unraveling the Truth Behind the Rumors

You may want to see also

![]()

Additional Benefits: Explore perks like loan discounts or payment flexibility for members

Navy Federal Credit Union members can unlock a suite of advantages when financing a used car, going beyond the standard loan process. One standout perk is the loan discount program, which can significantly reduce the overall cost of borrowing. For instance, members who set up automatic payments from their Navy Federal checking account may qualify for a 0.25% APR discount. This small percentage can translate to hundreds of dollars in savings over the life of the loan, especially for longer terms like 60 or 72 months. To maximize this benefit, ensure your checking account is active and meets the credit union’s eligibility criteria.

Another critical advantage is payment flexibility, designed to accommodate members’ unique financial situations. Navy Federal offers options like deferred payments for up to 90 days, ideal for those transitioning between jobs or awaiting military deployment. Additionally, members can choose bi-weekly payments to reduce interest accrual and pay off the loan faster. For example, a $20,000 loan at 4.99% APR could save over $500 in interest with bi-weekly payments compared to monthly payments. This flexibility ensures that members can align their loan structure with their cash flow needs without penalties.

A lesser-known but valuable perk is the vehicle protection plans available to Navy Federal members. These plans, such as extended warranties or GAP insurance, can be rolled into the loan, providing comprehensive coverage without upfront costs. For instance, GAP insurance covers the difference between the car’s value and the loan balance if the vehicle is totaled, a common concern with used cars. Members should evaluate these add-ons based on the vehicle’s age, mileage, and their risk tolerance, as they can offer peace of mind for a nominal monthly fee.

Lastly, Navy Federal’s relationship rewards program can further enhance savings for loyal members. Those with multiple accounts, such as credit cards or mortgages, may qualify for additional loan discounts or waived fees. For example, a member with a Navy Federal credit card and a savings account could receive a 0.10% APR reduction on their auto loan. To leverage this, consolidate your financial services with the credit union and inquire about eligibility for tiered benefits. This strategic approach ensures you’re maximizing every possible advantage as a member.

In summary, Navy Federal’s additional benefits—from loan discounts to payment flexibility and protective add-ons—transform the used car financing process into an opportunity for savings and security. By understanding and strategically utilizing these perks, members can drive away with a vehicle that fits both their budget and lifestyle. Always review the terms and conditions to ensure you’re fully capitalizing on these member-exclusive advantages.

Do Army and Navy Players Receive NIL Compensation? Exploring the Rules

You may want to see also

Frequently asked questions

Yes, Navy Federal offers used car loans for vehicles up to 15 years old, depending on the loan term and vehicle condition.

To qualify, you must be a Navy Federal member, meet their credit requirements, and provide details about the vehicle, such as its age, mileage, and condition.

Yes, Navy Federal provides pre-approval options for used car loans, which can help you understand your budget and negotiate better at the dealership.

Navy Federal finances most used cars, but vehicles must meet their criteria, including age, mileage, and condition. Salvaged or rebuilt vehicles may not qualify.