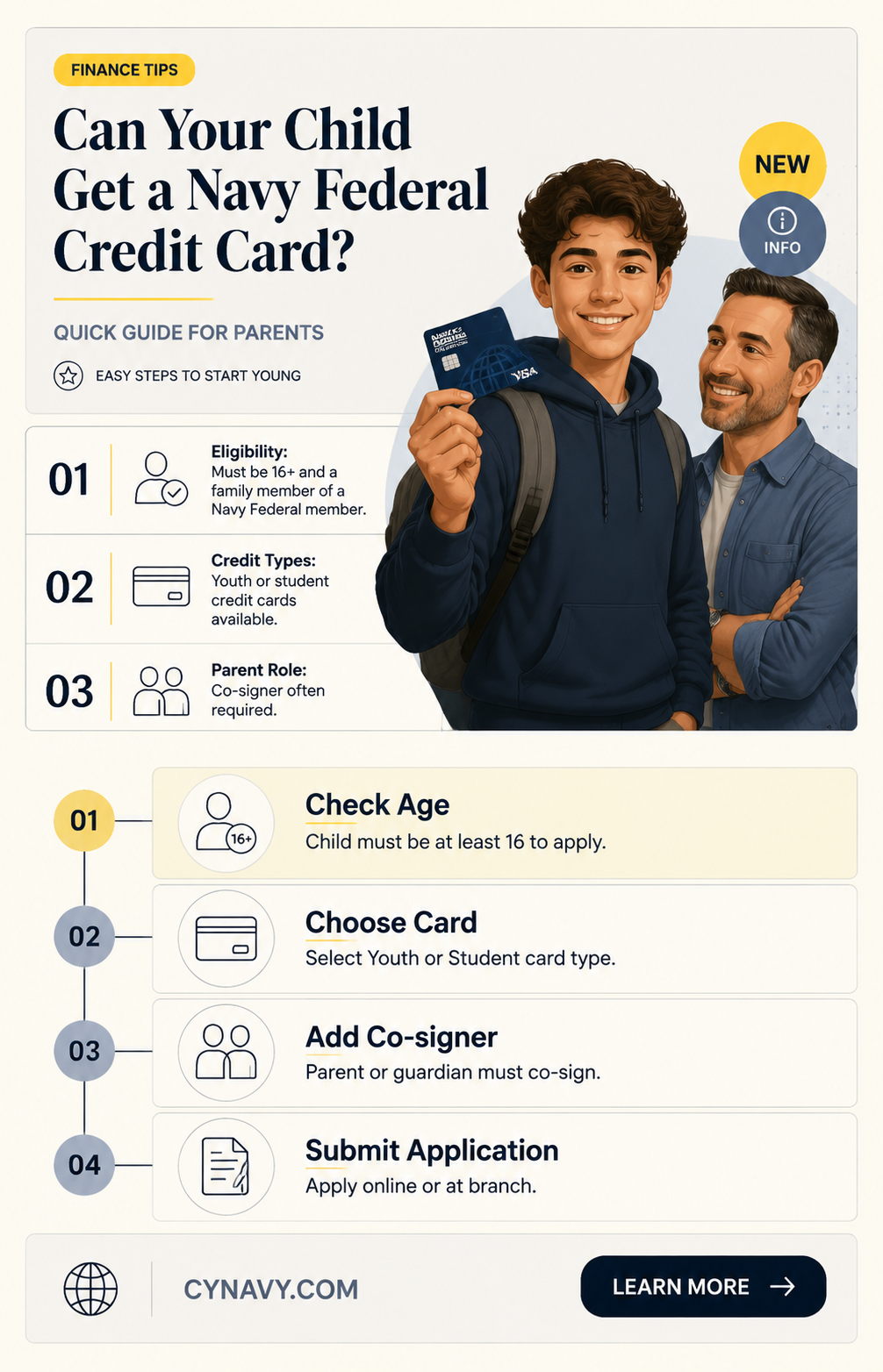

If you're considering getting your child a Navy Federal Credit Card, it's important to understand the options and requirements available through Navy Federal Credit Union. Navy Federal offers specific credit card products designed for young adults and dependents, such as the Navy Federal Credit Union’s Go Rewards Credit Card, which is tailored for individuals aged 18 and older. To qualify, your child must be a member of Navy Federal, which typically requires a familial or military connection. Additionally, you can add your child as an authorized user on your existing Navy Federal credit card, allowing them to build credit while you maintain control over the account. However, it’s crucial to weigh the benefits of early credit-building against the responsibility and financial education needed to ensure your child uses the card wisely. Always review the terms, fees, and eligibility criteria before making a decision.

| Characteristics | Values |

|---|---|

| Eligibility | Must be at least 14 years old and have a Navy Federal Credit Union (NFCU) joint account with a parent or guardian who is a primary member. |

| Account Type | Joint account required; child cannot have a solo account until age 18. |

| Credit Card Options | No dedicated "child" credit card; joint account holders may be added as authorized users on the parent/guardian's NFCU credit card. |

| Credit Building | Authorized user status may help build the child's credit history if the primary account holder maintains good credit habits. |

| Liability | Primary account holder (parent/guardian) is responsible for all transactions and payments. |

| Fees | Depends on the specific NFCU credit card; no additional fees for adding an authorized user. |

| Credit Limit | Determined by the primary account holder's creditworthiness and card terms. |

| Monitoring | Parents/guardians can monitor spending and set limits through NFCU's online banking or mobile app. |

| Educational Tools | NFCU offers financial education resources for youth, but no specific tools tied to authorized user status. |

| Age Limit for Solo Account | Child can apply for their own NFCU credit card at age 18, subject to approval. |

| Membership Requirement | At least one parent/guardian must be an NFCU member (e.g., military affiliation, DoD employee, or family member of an existing member). |

Explore related products

What You'll Learn

![]()

Eligibility Requirements for Minors

Navy Federal Credit Union offers credit cards to minors, but only as authorized users on a parent or guardian's account. This means your child cannot have their own standalone credit card until they are at least 21 years old, unless they can prove independent income. The Credit CARD Act of 2009 restricts credit card issuance to individuals under 21 without a cosigner or verifiable income.

Unlock Navy Federal Access Code: Simple Steps for Secure Login

You may want to see also

Explore related products

![]()

Joint Account Options with Parents

Navy Federal Credit Union offers joint account options that allow parents to co-own accounts with their children, providing a structured way to introduce financial responsibility. These accounts, such as joint checking or savings, enable both parties to deposit, withdraw, and manage funds collaboratively. For minors, a parent or guardian must be the primary account holder, ensuring oversight while allowing the child to actively participate in financial decisions. This setup is ideal for teaching budgeting, saving, and the basics of account management in a controlled environment.

One of the key benefits of joint accounts is the ability to build a child’s credit history indirectly. While the account itself isn’t a credit card, responsible use of a joint checking or savings account can demonstrate financial reliability, a trait lenders value. For instance, consistent deposits and avoidance of overdrafts reflect positively on the child’s financial behavior. Parents can also use these accounts to monitor spending habits and provide real-time guidance, turning everyday transactions into teachable moments.

However, joint accounts come with considerations. Both parties share equal access and responsibility, meaning a child’s mistakes—like unauthorized withdrawals or poor spending decisions—impact both account holders. Parents should establish clear rules and expectations, such as setting spending limits or requiring approval for large transactions. Additionally, it’s crucial to discuss the account’s purpose, whether it’s for everyday expenses, saving for a goal, or learning financial management, to ensure alignment.

For parents considering a joint account as a stepping stone to a credit card, Navy Federal’s secured credit card is a viable next step. By adding the child as an authorized user on this card, parents can help build their credit while maintaining control over spending limits. This approach combines the educational benefits of joint accounts with the credit-building potential of a card, offering a gradual transition to independent financial management. Always review Navy Federal’s eligibility and age requirements to ensure compliance.

Securing a Guaranteed Corpsman Role in the Navy: What You Need to Know

You may want to see also

Explore related products

![]()

Credit Card Types for Teens

Teens can’t get their own Navy Federal Credit Union (NFCU) credit card until they turn 18, but parents can add them as authorized users on their accounts. This setup allows teens to use the card under parental supervision, building their credit history while the primary account holder retains full responsibility. NFCU offers several card types suitable for this purpose, including the cashRewards card for straightforward cashback and the More Rewards American Express® Card for higher rewards on everyday spending. Choosing the right card depends on your teen’s spending habits and your financial goals.

Before adding your teen as an authorized user, consider their maturity level and financial literacy. Start with a low credit limit to minimize risk and use this opportunity to teach budgeting, tracking expenses, and understanding interest rates. For instance, set a rule that the card is only for emergencies or specific purchases, like gas or school supplies. Regularly review statements together to ensure responsible usage and address any mistakes early. This hands-on approach turns the credit card into a teaching tool rather than a liability.

Secured credit cards are another option for teens, though NFCU doesn’t offer them. These cards require a cash deposit, which typically becomes the credit limit, and are ideal for teens with no credit history. While NFCU’s authorized user option is more accessible for members, secured cards from other institutions can still help teens build credit independently. Compare fees, interest rates, and reporting practices before choosing one, as not all secured cards report to the three major credit bureaus.

Prepaid debit cards are often marketed as alternatives to credit cards for teens, but they don’t build credit. However, they can be useful for teaching basic money management without the risk of debt. NFCU’s prepaid options, like the Navy Federal Debit Card for teens on a joint account, allow parents to monitor spending and set allowances. Pairing a prepaid card with financial education can prepare teens for eventual credit card use, ensuring they understand the difference between spending their own money and borrowing.

Ultimately, the best credit card type for your teen depends on their age, financial readiness, and your involvement. Authorized user status on an NFCU card is a practical choice for members, while secured cards or prepaid options offer alternatives for different needs. Regardless of the method, the goal is to instill financial responsibility and prepare teens for a future where credit plays a significant role. Start small, stay involved, and use every transaction as a learning opportunity.

How to Access Cash Using Your Navy Federal Credit Card

You may want to see also

Explore related products

![]()

Parental Control Features Available

Navy Federal Credit Union offers a range of financial products designed to help parents teach their children responsible money management. One of the key concerns for parents considering a credit card for their child is the ability to maintain oversight and control. Navy Federal addresses this through several parental control features embedded in their youth-oriented accounts. These tools are not just about restriction but also about education, allowing parents to guide their children’s financial decisions while gradually granting them independence.

For starters, parents can set spending limits on their child’s Navy Federal credit card. This feature ensures that children cannot overspend beyond a predetermined amount, helping them stay within a budget. For instance, if a parent wants their teenager to use the card only for school supplies or emergencies, they can cap the monthly limit at $200. This not only prevents financial mishaps but also teaches the value of living within means. Additionally, parents can receive real-time alerts whenever the card is used, providing immediate visibility into their child’s spending habits.

Another critical feature is the ability to monitor transactions through online banking or the mobile app. Parents can review purchase details, including dates, amounts, and merchant names, ensuring transparency. This monitoring capability is particularly useful for identifying unauthorized or suspicious activity. For example, if a child’s card is used at an unfamiliar location, the parent can investigate promptly. This level of oversight fosters trust while still allowing children to learn from their financial decisions.

Navy Federal also allows parents to add or remove funds from the linked account instantly. This flexibility ensures that children always have access to funds when needed, whether for an unexpected expense or as a reward for responsible behavior. Parents can also temporarily freeze the card if it’s lost or if they notice unusual activity, providing an added layer of security. These controls are especially beneficial for younger teens (ages 13–16) who are just beginning to navigate financial independence.

Finally, the credit card can be paired with educational resources provided by Navy Federal, such as financial literacy modules and budgeting tools. Parents can use these resources to discuss spending habits, savings goals, and the importance of credit scores with their children. By combining parental controls with educational opportunities, Navy Federal empowers both parents and children to make informed financial decisions. This holistic approach ensures that the credit card becomes a tool for learning rather than just a means of spending.

Joining the Navy SEALs: Essential Steps to Achieve Your Elite Dream

You may want to see also

Explore related products

![]()

Building Child’s Credit Early Tips

Establishing a solid credit history for your child early on can set them up for financial success in adulthood. One common question parents have is whether they can get their child a Navy Federal Credit Card. While Navy Federal offers options for minors, such as joint accounts or authorized user status, the focus should be on strategies that build credit responsibly. Here’s how to approach this effectively.

Start with a Joint Checking or Savings Account

Before diving into credit, introduce your child to basic banking through a joint checking or savings account. Navy Federal allows parents to open accounts for minors as young as 13, teaching them about money management, budgeting, and financial responsibility. This foundational step ensures they understand the value of money before handling credit. Use this opportunity to discuss transactions, fees, and the importance of balancing an account—skills that translate directly to credit management.

Add Your Child as an Authorized User

Once your child is ready, consider adding them as an authorized user on your Navy Federal credit card. This strategy allows their credit profile to benefit from your responsible usage, as the account activity is reported to the credit bureaus. However, proceed with caution: ensure your own credit habits are impeccable, as negative behavior (late payments, high balances) will also reflect on their report. Start this process when your child is at least 15–16 years old, giving them time to observe and learn before managing credit independently.

Encourage Responsible Usage and Monitoring

If your child is an authorized user, limit their access to the card or set clear boundaries on usage. For instance, allow them to use the card for small, recurring expenses like gas or subscriptions, ensuring they understand the importance of paying off balances in full each month. Teach them to monitor their credit report annually via free services like AnnualCreditReport.com, instilling a habit of financial vigilance. This hands-on approach not only builds credit but also fosters accountability.

Explore Secured Credit Cards as a Next Step

Once your child turns 18, they may qualify for a secured credit card through Navy Federal, which requires a cash deposit as collateral. This option is ideal for young adults with no credit history, as it minimizes risk for the lender while allowing them to build credit independently. Encourage them to keep the balance below 30% of the limit and pay on time, demonstrating responsible credit behavior. Pair this with ongoing conversations about credit scores, interest rates, and long-term financial goals.

By combining these strategies, you can help your child establish a strong credit foundation while leveraging Navy Federal’s offerings. The key is to balance opportunity with education, ensuring they develop healthy financial habits that last a lifetime.

Navy Federal Cashier's Check Guide: Easy Steps to Obtain Yours

You may want to see also

Frequently asked questions

Yes, as a Navy Federal Credit Union member, you can add your child as a joint owner or authorized user on your account, allowing them to have a card under your supervision.

Navy Federal does not specify a minimum age for authorized users, but your child must be old enough to sign their name on the card, typically around 13–14 years old.

If your child is added as a joint owner, their credit activity may be reported to the credit bureaus, helping them build credit. However, authorized users typically do not build credit unless explicitly reported.

Navy Federal does not charge additional fees for adding authorized users or joint owners to your credit card account. However, you remain responsible for all charges made by your child.