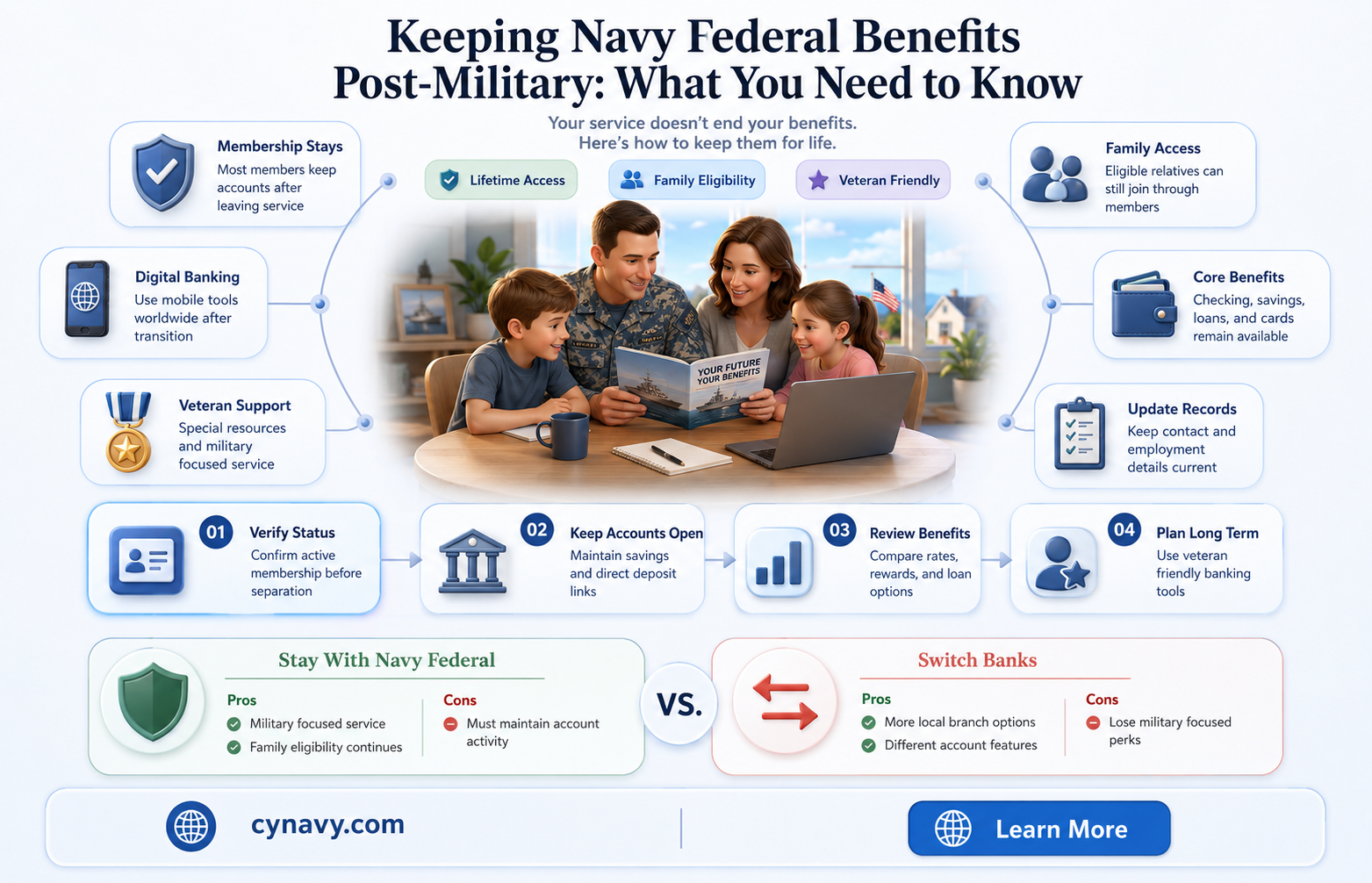

Leaving the military often raises questions about the continuity of certain benefits, including banking services. One common concern is whether you can retain your Navy Federal Credit Union (NFCU) membership after separation from the armed forces. Navy Federal is known for its exclusive membership requirements, primarily serving military personnel, veterans, and their families. Fortunately, NFCU allows former military members to maintain their accounts and continue accessing its services even after they transition to civilian life. This means you can keep your Navy Federal account, enjoying the benefits of their financial products and services without interruption, ensuring a seamless financial transition post-military.

| Characteristics | Values |

|---|---|

| Membership Eligibility After Separation | Yes, you can keep your Navy Federal Credit Union (NFCU) membership after leaving the military. |

| Eligibility Requirements | Must have been a member in good standing at the time of separation. |

| Account Types Retained | Checking, savings, credit cards, loans, and other financial products. |

| Joint Accounts | Joint account holders (e.g., spouses or family members) can retain membership if they meet eligibility criteria. |

| Family Membership | Immediate family members (spouse, children, siblings, etc.) can retain or establish membership. |

| Retired Military | Retired military members retain full membership benefits. |

| Veterans | Veterans who were members while serving can keep their membership. |

| Civilian Employees | Civilian employees of the Department of Defense (DoD) or military installations can retain membership. |

| Account Closure | No automatic closure of accounts upon separation; accounts remain active unless closed by the member. |

| Membership Benefits | Continued access to competitive rates, low fees, and exclusive member perks. |

| Online and Mobile Banking | Full access to online and mobile banking services. |

| Branch Access | Access to NFCU branches and ATMs, though availability may depend on location. |

| Customer Service | Continued access to NFCU customer service and support. |

| New Membership Applications | Former military members cannot reapply if membership is terminated after separation. |

| Membership Termination | Membership may be terminated if eligibility criteria are not met (e.g., no eligible family member or account activity). |

| Updates Required | Ensure contact and account information is updated to avoid service disruptions. |

Explore related products

What You'll Learn

![]()

Eligibility for Former Military Members

Former military members often wonder if their relationship with Navy Federal Credit Union ends when their service does. The good news is, it doesn't have to. Navy Federal offers a lifetime membership benefit, meaning once you're in, you're in for life, regardless of your military status. This perk is a significant advantage, as it allows veterans to continue accessing the credit union's services, including competitive loan rates, low-fee banking, and specialized financial products tailored to military life.

To maintain eligibility, former military members must ensure their accounts remain active. This can be achieved through regular transactions, such as direct deposits, bill payments, or even small monthly transfers. It's a simple yet crucial step to preserve the benefits of membership. Navy Federal also encourages members to update their contact information post-separation to ensure uninterrupted access to services and important communications.

One of the most appealing aspects of retaining Navy Federal membership is the continuity of financial services. Veterans can continue to use their existing accounts, credit cards, and loans without the hassle of switching institutions. This stability is particularly valuable during the transition to civilian life, a period often marked by significant changes and financial adjustments. For instance, Navy Federal's personal loans and mortgage options, designed with military personnel in mind, can be a lifeline for veterans looking to establish themselves in the civilian housing market.

However, it's essential to understand that while membership continues, certain benefits may change. For example, some military-specific promotions or discounts might no longer apply. Veterans should review their account details and benefits post-separation to fully understand what remains available to them. Navy Federal's customer service team is a valuable resource for clarifying any changes and exploring new opportunities tailored to veteran status.

In summary, former military members can indeed keep their Navy Federal membership after leaving the service, provided they maintain an active account. This lifelong benefit offers financial stability and access to specialized services, making it a valuable asset for veterans navigating post-military life. By staying engaged with their accounts and keeping their information updated, veterans can continue to leverage the advantages of Navy Federal membership, ensuring a smooth financial transition into civilian life.

How to Access Cash Using Your Navy Federal Credit Card

You may want to see also

Explore related products

![]()

Account Types Available Post-Service

Separating from the military doesn’t mean losing access to Navy Federal Credit Union’s robust financial ecosystem. While membership eligibility shifts post-service, the credit union offers a range of account types tailored to veterans and retirees, ensuring continuity in financial management. From everyday checking to long-term savings, these accounts are designed to meet diverse needs, often with benefits like waived fees and competitive rates. Understanding which accounts remain accessible—and how to qualify—is key to maximizing your financial strategy after service.

Checking Accounts: Seamless Transitions for Daily Banking

Navy Federal’s checking accounts, such as the Free Active Duty Checking and Free Easy Checking, remain available post-service, though account names and features may adjust. For instance, Free Active Duty Checking transitions to Free Easy Checking, retaining perks like no monthly fees and free ATM access. Veterans can also upgrade to Flagship Checking, which offers higher interest rates on balances over $1,500, ideal for those with steady income streams. Pro tip: Set up direct deposit for your VA benefits or pension to maintain fee-free status and streamline cash flow.

Savings Accounts: Building Reserves Beyond the Uniform

Post-service, savings options like the Basic Savings Account (which establishes membership) and Certificate Accounts (CDs) remain accessible. The Basic Savings Account acts as a gateway to other products, requiring just $5 to maintain membership. For longer-term goals, Navy Federal’s CDs offer competitive rates, with terms ranging from 3 months to 7 years. Veterans can also leverage the Certificate Secured Loan, using CD funds as collateral for low-interest loans, a smart strategy for rebuilding credit or funding transitions.

Investment and Retirement Accounts: Planning for the Long Haul

Navy Federal’s brokerage services, powered by Navy Federal Investment Services, allow veterans to continue growing wealth through IRAs, mutual funds, and managed portfolios. Roth IRAs are particularly advantageous for post-service life, offering tax-free withdrawals in retirement. For those nearing separation, rolling military TSP funds into a Navy Federal IRA can provide more control and investment options. Caution: Consult a financial advisor to avoid tax penalties during rollovers.

Credit Cards and Loans: Financial Flexibility Post-Service

Veterans retain access to Navy Federal’s credit cards, such as the cashRewards card (1.5% cashback) and the More Rewards American Express Card (3x points on travel). Loan products, including personal loans and mortgages, also remain available, often with preferential rates for former service members. For example, the VA Home Loan program, facilitated by Navy Federal, offers 0% down payment options—a significant benefit for transitioning to civilian homeownership.

In summary, Navy Federal’s post-service account offerings provide a comprehensive financial toolkit for veterans. By strategically selecting accounts—from no-fee checking to retirement-focused investments—former service members can maintain financial stability and growth long after their military careers end. The key lies in understanding eligibility criteria and leveraging tailored benefits to align with post-service goals.

Navy Federal Car Insurance: Coverage Options and Benefits Explained

You may want to see also

Explore related products

![]()

Membership Retention Requirements

Leaving the military doesn't automatically sever your relationship with Navy Federal Credit Union. Their membership retention policy is designed with flexibility, recognizing the diverse paths veterans and former service members take.

Eligibility Extensions: Once you've established membership, Navy Federal doesn't require active duty status for continued eligibility. This means retirees, honorably discharged veterans, and even family members of current or former members can maintain their accounts.

Think of it like a lifelong club membership – your initial connection grants you ongoing access to the benefits.

Account Activity: While eligibility persists, keeping your account active is crucial. Regular transactions, direct deposits, or maintaining a minimum balance (typically $5) are common ways to ensure your account remains open. Think of it as nurturing a plant – occasional attention keeps it thriving.

Navy Federal may reach out if your account becomes dormant, offering solutions to prevent closure.

Communication is Key: Navy Federal values its members, especially those with military ties. If you're transitioning out of the service, proactively contact them. They can guide you through any necessary updates to your account information and ensure a seamless continuation of your membership.

Beyond Banking: Navy Federal understands the unique financial needs of military families. Their commitment to veterans extends beyond account retention. They offer specialized loan programs, financial education resources, and community support tailored to the post-military experience.

Aspergers, ADHD, and Navy Service: Exploring Eligibility and Opportunities

You may want to see also

Explore related products

![]()

Benefits for Veterans and Families

Veterans transitioning to civilian life often worry about losing access to financial institutions that understand their unique needs. Navy Federal Credit Union (NFCU), however, stands out by allowing former military members to retain their accounts and benefits, even after separation or retirement. This continuity provides a critical financial anchor during a period of significant change, ensuring veterans and their families can maintain stability without the added stress of switching banks.

One of the most valuable benefits NFCU offers veterans is access to specialized loan programs. For instance, the Veterans Affairs (VA) mortgage program, available through NFCU, provides 100% financing with no private mortgage insurance (PMI) requirement. This can save veterans thousands of dollars over the life of a loan. Additionally, NFCU offers competitive rates on auto loans, personal loans, and credit cards, often with more flexible terms for veterans. These financial tools can be particularly beneficial for families adjusting to a single income or pursuing new career paths.

Beyond loans, NFCU provides veterans with financial education resources tailored to their post-military life. Workshops and online courses cover topics like budgeting on a civilian salary, managing debt, and planning for retirement. For families, this education is invaluable, as it helps bridge the gap between military and civilian financial systems. NFCU also offers free credit counseling services, which can be a lifeline for veterans navigating the complexities of civilian credit scores and financial planning.

Another standout feature is NFCU’s commitment to supporting military families. Spouses and dependents of veterans retain membership eligibility, ensuring the entire family can benefit from NFCU’s services. This includes access to youth savings accounts, scholarships, and financial literacy programs for children. For families relocating after military service, NFCU’s extensive ATM network and online banking tools provide seamless financial management, regardless of location.

In conclusion, NFCU’s benefits for veterans and their families go beyond mere account retention. By offering specialized loans, financial education, and family-focused services, NFCU ensures veterans can build a secure financial future. This holistic approach not only honors their service but also empowers them to thrive in civilian life. For veterans wondering if they can keep Navy Federal after leaving the military, the answer is a resounding yes—and the benefits are well worth holding onto.

How to Access Your Pending Deposit Early with Navy Federal

You may want to see also

Explore related products

![]()

Closing or Transferring Accounts

Leaving the military often prompts a reevaluation of financial ties, including banking relationships. For those who’ve relied on Navy Federal Credit Union (NFCU), the question of whether to close or transfer accounts arises. Closing an account is straightforward but final—it severs all ties with NFCU, eliminating access to their services. This option is ideal if you’re moving to a new financial institution with better terms or if you no longer meet NFCU’s eligibility requirements. However, it’s irreversible, so ensure you’ve settled all pending transactions and withdrawn funds before proceeding.

Transferring accounts, on the other hand, allows you to retain your NFCU membership while adjusting your account structure. For instance, you might transfer a joint account to an individual one or shift funds from a checking to a savings account. This approach is practical if you value NFCU’s benefits, such as competitive rates or customer service, but need to adapt your banking setup to your post-military lifestyle. Be aware that certain account types, like military-specific products, may require modifications to comply with eligibility rules.

Before deciding, weigh the pros and cons of each option. Closing an account offers a clean break but forfeits NFCU’s lifetime membership benefits. Transferring accounts preserves your relationship with NFCU but may require adjustments to maintain eligibility. For example, if you’re no longer affiliated with the military, you’ll need a family member who is eligible to sponsor your membership. Alternatively, maintaining a basic savings account with a minimum balance can keep your membership active.

Practical steps include contacting NFCU to discuss your options and any fees associated with closing or transferring accounts. If closing, ensure all direct deposits and automatic payments are redirected to avoid disruptions. If transferring, verify which accounts qualify and whether any documentation is needed. For instance, transferring a joint account may require consent from all account holders.

Ultimately, the decision hinges on your financial goals and post-military circumstances. If you prioritize flexibility and are confident in your new financial institution, closing might be the way to go. If NFCU’s benefits align with your long-term needs, transferring accounts ensures continuity while adapting to your new life chapter. Either way, proactive planning ensures a smooth transition without compromising your financial stability.

Navy Federal Direct Deposit: How to Get Your Paycheck Early

You may want to see also

Frequently asked questions

Yes, you can keep your Navy Federal Credit Union account even after you leave the military. Once you become a member, your membership is for life, regardless of your military status.

Yes, it’s important to update your account information, including your contact details and employment status, to ensure you continue receiving all member benefits and communications from Navy Federal.

While your core membership remains, eligibility for certain products (e.g., military-specific loans or rates) may change. However, Navy Federal offers a wide range of products for all members, including veterans and civilians.

Yes, eligible family members can still maintain their Navy Federal accounts and benefits even if you leave the military, as long as they were added as joint owners or account holders during your active membership.