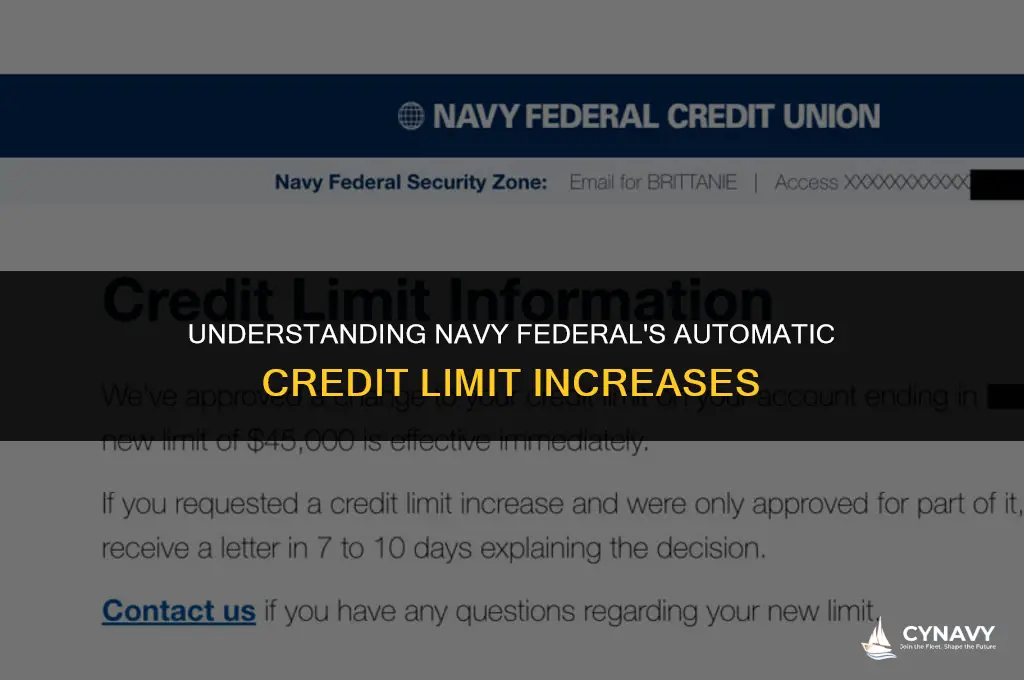

Navy Federal Credit Union is known for its customer-centric approach, which includes periodically reviewing and potentially increasing the credit limits of its cardholders. This automatic credit limit increase is typically based on several factors, including the cardholder's payment history, credit utilization ratio, and overall creditworthiness. Cardholders who demonstrate responsible credit behavior, such as making timely payments and keeping their credit utilization low, may be more likely to receive an automatic credit limit increase. Navy Federal aims to provide its members with financial flexibility and rewards for maintaining good credit habits.

| Characteristics | Values |

|---|---|

| Automatic Increase Frequency | Typically every 6-12 months |

| Increase Amount | Varies, often $500-$1,000 |

| Eligibility Criteria | Good payment history, sufficient income |

| Notification Method | Email or account statement |

| Opt-Out Option | Yes, via online banking or phone |

| Impact on Credit Score | Temporary decrease due to credit inquiry |

| Frequency of Review | Annually or upon request |

Explore related products

What You'll Learn

- Factors Influencing Increases: Account age, payment history, income, credit utilization ratio, and overall creditworthiness

- Frequency of Reviews: Navy Federal may review credit limits every 6-12 months or upon request

- Automatic vs. Manual Increases: Automatic increases based on predefined criteria; manual increases require member request and additional verification

- Credit Limit Caps: Maximum credit limits vary by card type and individual credit profiles

- Notifications and Monitoring: Members may receive notifications of credit limit changes; regular monitoring of credit reports is recommended

![]()

Factors Influencing Increases: Account age, payment history, income, credit utilization ratio, and overall creditworthiness

Navy Federal Credit Union, like many financial institutions, periodically reviews its members' credit limits to determine if an increase is warranted. Several key factors influence this decision, each providing insight into a member's creditworthiness and financial stability.

Account age is a significant consideration. Longer-standing accounts demonstrate a member's commitment to the credit union and provide a more extensive history for evaluation. Payment history is equally crucial; consistent, on-time payments indicate responsible credit management and reduce the perceived risk of default.

Income plays a vital role in credit limit assessments. Higher income levels generally suggest a greater capacity to repay debts, although this must be balanced against other financial obligations and expenses. Credit utilization ratio, which compares the amount of credit used to the total credit available, is another critical factor. Lower utilization ratios indicate that a member is not overextending themselves financially and may have room for additional credit.

Lastly, overall creditworthiness is evaluated, encompassing factors such as credit scores, debt-to-income ratios, and public records like bankruptcies or liens. This comprehensive assessment helps Navy Federal determine the likelihood of a member defaulting on their debts and guides decisions on credit limit increases.

In summary, Navy Federal considers a combination of account age, payment history, income, credit utilization ratio, and overall creditworthiness when deciding on automatic credit limit increases. Each factor provides valuable information about a member's financial health and ability to manage additional credit responsibly.

Understanding the Navy Federal Credit Union CU Card: Benefits and Features

You may want to see also

Explore related products

![]()

Frequency of Reviews: Navy Federal may review credit limits every 6-12 months or upon request

Navy Federal Credit Union conducts periodic reviews of its members' credit limits to ensure they align with the members' financial situations and creditworthiness. These reviews typically occur every 6 to 12 months, depending on various factors such as the member's credit history, account activity, and overall financial health. The frequency of these reviews is a critical aspect of Navy Federal's approach to managing credit limits, as it allows the credit union to make informed decisions about potential credit limit increases or decreases.

During these reviews, Navy Federal may consider a range of factors, including the member's payment history, credit utilization ratio, and any changes in their income or employment status. The credit union may also review the member's overall debt-to-income ratio and credit score to assess their creditworthiness. Based on this information, Navy Federal may decide to automatically increase a member's credit limit if they demonstrate responsible credit behavior and meet the credit union's criteria.

In addition to these periodic reviews, Navy Federal may also review a member's credit limit upon request. This means that if a member believes their credit limit should be increased or decreased, they can contact Navy Federal and request a review. During this process, the member may be asked to provide additional information or documentation to support their request, such as proof of income or employment.

It's important to note that Navy Federal's credit limit reviews are not solely focused on increasing credit limits. In some cases, the credit union may decide to decrease a member's credit limit if they exhibit risky credit behavior or if their financial situation has deteriorated. This approach helps Navy Federal manage risk and ensure that its members are not overextending themselves financially.

Overall, Navy Federal's frequency of credit limit reviews is designed to strike a balance between providing members with the credit they need and managing risk. By conducting regular reviews and considering a range of factors, Navy Federal can make informed decisions about credit limit adjustments that are in the best interests of its members.

Exploring Early Deposit Release Options with Navy Federal

You may want to see also

Explore related products

![]()

Automatic vs. Manual Increases: Automatic increases based on predefined criteria; manual increases require member request and additional verification

Navy Federal Credit Union offers both automatic and manual credit limit increases, each with its own set of criteria and processes. Automatic increases are typically based on predefined criteria such as payment history, credit utilization, and overall creditworthiness. These increases are periodically reviewed and granted without the need for the member to initiate a request. This can be beneficial for members who consistently demonstrate responsible credit behavior, as it allows for a seamless increase in their credit limit without additional effort.

On the other hand, manual increases require the member to request a credit limit increase and undergo additional verification. This process may involve providing updated financial information, such as income and employment details, as well as explaining the reason for the requested increase. Manual increases can be advantageous for members who have experienced significant changes in their financial situation that may not be reflected in their credit report, allowing them to potentially qualify for a higher credit limit.

When comparing automatic and manual increases, it's important to consider the frequency and potential impact of each type. Automatic increases may occur more frequently, as they are based on ongoing monitoring of the member's credit behavior. However, manual increases can result in more substantial credit limit increases, as they take into account a broader range of financial factors. Members should weigh the convenience of automatic increases against the potential benefits of manual increases when deciding which option best suits their needs.

In conclusion, Navy Federal Credit Union's approach to credit limit increases provides members with both automatic and manual options, catering to different preferences and financial situations. By understanding the criteria and processes associated with each type of increase, members can make informed decisions about managing their credit limits effectively.

Step-by-Step Guide to Closing Your Navy Federal Checking Account

You may want to see also

Explore related products

![]()

Credit Limit Caps: Maximum credit limits vary by card type and individual credit profiles

Credit limit caps are a crucial aspect of credit card usage, as they dictate the maximum amount a cardholder can spend before reaching their credit limit. These caps vary significantly depending on the type of card and the individual's credit profile. For instance, premium credit cards often come with higher credit limits compared to standard or secured cards. Similarly, individuals with excellent credit scores and a strong credit history are more likely to be approved for higher credit limits than those with poor or limited credit.

Navy Federal Credit Union, like many other financial institutions, periodically reviews cardholders' accounts to determine if they are eligible for a credit limit increase. This process typically involves assessing the cardholder's payment history, credit utilization ratio, and overall creditworthiness. If a cardholder demonstrates responsible credit behavior, such as making timely payments and keeping their credit utilization low, they may be considered for a credit limit increase.

However, it's important to note that credit limit increases are not automatic and are subject to Navy Federal's underwriting criteria. Cardholders may need to request a credit limit increase manually, either through their online account or by contacting Navy Federal's customer service. The frequency of these requests and the likelihood of approval will depend on various factors, including the cardholder's credit profile and the specific terms and conditions of their credit card agreement.

In some cases, Navy Federal may proactively offer a credit limit increase to cardholders who have demonstrated exemplary credit behavior. This can be a strategic move to encourage cardholders to continue using their cards responsibly and to potentially increase their spending. However, cardholders should always be mindful of their credit limits and avoid overspending, as exceeding their credit limit can result in fees and negatively impact their credit score.

Ultimately, understanding credit limit caps and how they are determined is essential for cardholders to manage their finances effectively. By maintaining a good credit profile and demonstrating responsible credit behavior, cardholders can increase their chances of being approved for higher credit limits, which can provide greater financial flexibility and convenience.

Exploring Early Fund Release Options with Navy Federal

You may want to see also

Explore related products

![]()

Notifications and Monitoring: Members may receive notifications of credit limit changes; regular monitoring of credit reports is recommended

Members of Navy Federal Credit Union may receive notifications regarding changes to their credit limit. These notifications can be a valuable tool for staying informed about the status of your credit account. It's important to note that these notifications are not always indicative of an automatic credit limit increase. They could also inform you of a decrease or no change at all. Regular monitoring of your credit reports is recommended to ensure you are aware of any changes and can take appropriate action if necessary.

Credit limit changes can be influenced by a variety of factors, including your payment history, credit utilization ratio, and overall creditworthiness. Navy Federal may automatically increase your credit limit if they observe positive behavior, such as timely payments and responsible credit usage. However, it's crucial to remember that this is not guaranteed and depends on their internal policies and your individual financial situation.

To effectively monitor your credit reports, you should obtain a copy of your report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) at least once a year. You can do this for free through AnnualCreditReport.com. When reviewing your reports, look for any discrepancies or errors and dispute them if necessary. Also, pay attention to your credit utilization ratio, which is the amount of credit you're using compared to the amount available to you. Keeping this ratio low can positively impact your credit score and may lead to automatic credit limit increases.

In addition to monitoring your credit reports, you should also be mindful of your spending habits and credit usage. Avoid maxing out your credit cards and try to pay off your balances in full each month. This demonstrates responsible credit behavior and can increase your chances of an automatic credit limit increase. Furthermore, consider setting up alerts with Navy Federal to notify you of any significant changes to your account, including credit limit adjustments.

In conclusion, while Navy Federal may automatically increase your credit limit based on their assessment of your creditworthiness, it's essential to stay proactive in monitoring your credit reports and maintaining responsible credit habits. By doing so, you can ensure you're aware of any changes to your credit limit and can take steps to improve your financial standing.

Will Navy Federal Release Your Tax Refund Early? Find Out Here!

You may want to see also

Frequently asked questions

Navy Federal may automatically increase your credit limit periodically, typically every 6 to 12 months, based on your account activity and creditworthiness.

Factors that can influence Navy Federal's decision to automatically increase your credit limit include your payment history, credit utilization ratio, overall credit score, and the length of time you've had the account.

Yes, you can request a credit limit increase from Navy Federal at any time. You can do this by contacting their customer service or through their online banking platform. They will review your request based on your account history and creditworthiness.