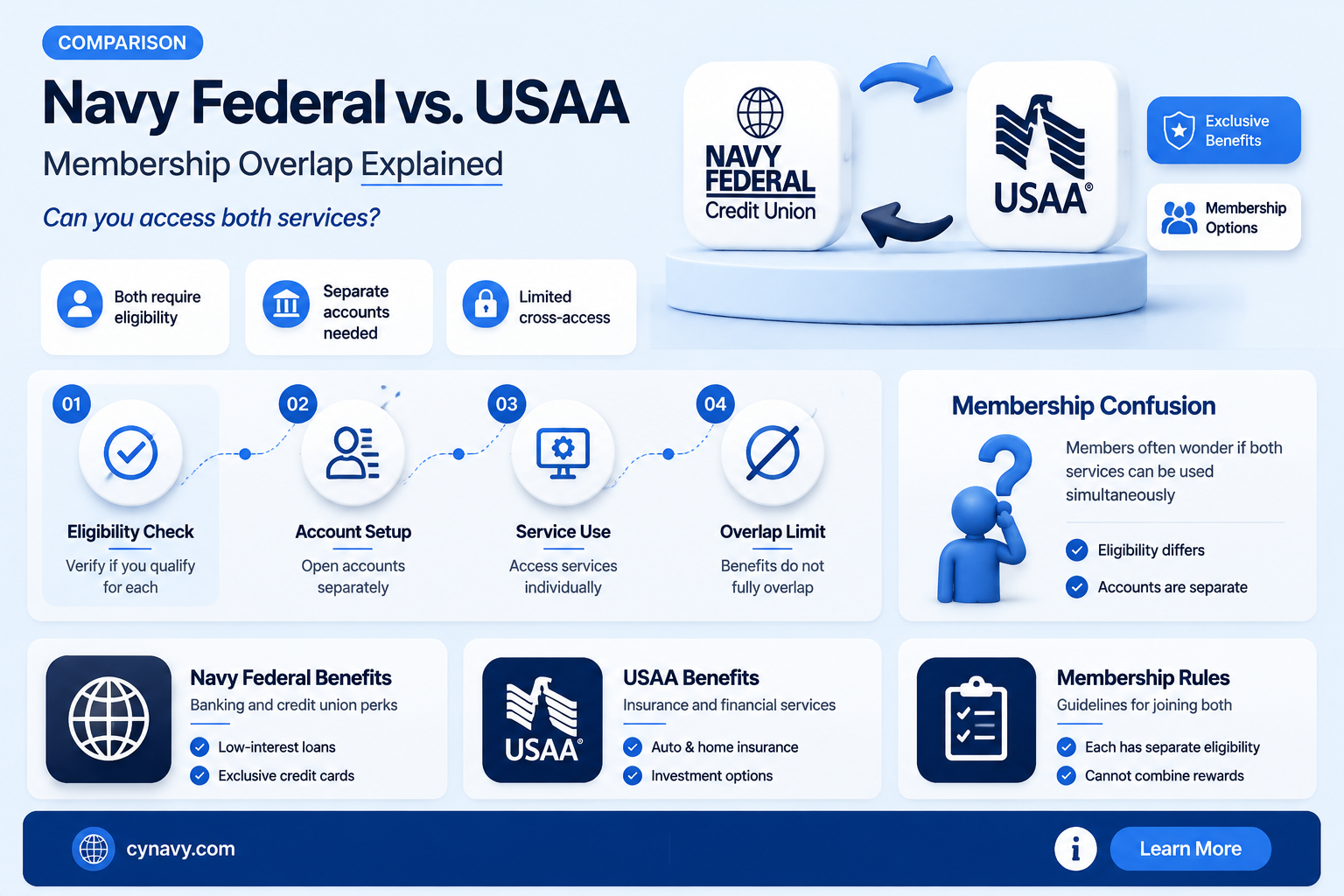

The question of whether a member of Navy Federal Credit Union (NFCU) can also join USAA (United Services Automobile Association) is a common one, as both institutions cater to military personnel and their families. While NFCU is a credit union exclusively serving active-duty military, veterans, and their families, USAA is a financial services company offering insurance, banking, and investment products to a similar demographic. Although membership in one does not automatically grant eligibility for the other, individuals who qualify for NFCU—such as active-duty military, veterans, and certain family members—often meet USAA’s eligibility criteria as well. However, it’s essential to verify specific requirements for USAA membership, as they may include additional criteria beyond military affiliation. Ultimately, many individuals find value in utilizing services from both institutions to meet their diverse financial needs.

| Characteristics | Values |

|---|---|

| Eligibility for USAA Membership | USAA membership is generally limited to active, retired, and honorably separated members of the U.S. military, along with their eligible family members. |

| Navy Federal Credit Union (NFCU) Membership | NFCU membership is open to active duty, retired, and veterans of the U.S. Armed Forces, along with their families, and Department of Defense (DoD) civilians. |

| Overlap in Eligibility | There is significant overlap in eligibility between NFCU and USAA, as both serve military personnel and their families. |

| Dual Membership | Members of NFCU can also be eligible for USAA membership if they meet USAA's specific eligibility criteria (e.g., military affiliation). |

| Services Offered | Both NFCU and USAA offer financial services such as banking, loans, insurance, and investment products, but they are separate entities with distinct offerings. |

| Membership Requirements | USAA requires proof of military affiliation for membership, while NFCU requires a connection to the military or DoD. |

| Application Process | Eligible individuals can apply for USAA membership independently of their NFCU membership by providing necessary documentation. |

| Benefits Comparison | USAA is known for its insurance products, while NFCU is recognized for competitive rates on loans and credit cards. |

| Geographic Availability | Both institutions offer services nationwide and internationally, catering to military members and their families. |

| Independence of Institutions | NFCU and USAA are separate organizations, and membership in one does not automatically grant membership in the other. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for USAA Membership

USAA membership is highly sought after for its comprehensive financial services, but not everyone qualifies. The eligibility criteria are specific and rooted in the organization’s military-focused mission. To join USAA, you must fall into one of several distinct categories tied to military service or family connections. Here’s a breakdown of who qualifies and how Navy Federal Credit Union (NFCU) members fit into this framework.

Military Affiliation as the Core Requirement

USAA’s primary eligibility criterion is a direct connection to the U.S. military. Active-duty members, veterans, and retirees of any branch—Army, Navy, Air Force, Marines, Coast Guard, or National Guard—automatically qualify. This includes those who have served honorably, even if their service was brief. For example, a sailor who completed a four-year enlistment in the Navy would meet this requirement. Importantly, membership is not limited to current service members; veterans who separated decades ago remain eligible, provided they can verify their service.

Family Ties Extend Eligibility

Beyond individual service, USAA extends membership to immediate family members of eligible military personnel. Spouses, children, and widows/widowers of those who served or are currently serving qualify. For instance, if a Navy FCU member is married to an Army veteran, they can join USAA through their spouse’s eligibility. However, siblings, cousins, or in-laws do not qualify based on familial relationships alone. Documentation, such as a marriage certificate or military discharge papers, is typically required to verify these connections.

Navy FCU Membership Alone Is Insufficient

Being a member of Navy Federal Credit Union does not automatically grant eligibility for USAA. While both institutions cater to military communities, their membership criteria differ. Navy FCU requires a Department of Defense affiliation—such as active-duty service, veteran status, or being a family member—but USAA’s requirements are more specific. A Navy FCU member who is a civilian employee of the DoD, for example, would not qualify for USAA unless they meet one of the military-related criteria outlined above.

Practical Steps for Navy FCU Members

If you’re a Navy FCU member wondering about USAA eligibility, start by assessing your military connection. If you’ve served, gather your DD-214 or other discharge documents. If you’re a spouse or child, collect proof of your relationship to the eligible service member. USAA’s website offers a straightforward eligibility checker, which can clarify your status in minutes. For those without direct military ties, consider other financial institutions with similar benefits, as USAA’s membership remains exclusive to its defined community.

Takeaway: Eligibility Hinges on Military Service or Family Ties

While Navy FCU and USAA both serve military families, USAA’s eligibility criteria are narrower and non-negotiable. Membership is a privilege reserved for those with a direct military connection or their immediate family. For Navy FCU members, the key to unlocking USAA’s services lies in verifying their military affiliation—whether through personal service or a qualifying relationship. Without this, USAA remains out of reach, but alternative financial options tailored to military communities are available.

Joining Navy Federal: Eligibility, Application, and Membership Benefits Explained

You may want to see also

Explore related products

![]()

Navy Federal vs. USAA Benefits

Membership in Navy Federal Credit Union (NFCU) and USAA offers distinct advantages, but they cater to different needs and eligibility criteria. While NFCU is a credit union primarily serving military members and their families, USAA is an insurance and financial services company with a similar focus. A key question arises: Can a member of Navy Federal also access USAA benefits? The answer is yes, but with specific conditions. USAA requires military affiliation, which many NFCU members already meet. However, USAA’s eligibility extends to veterans, retirees, and certain family members, whereas NFCU’s membership is broader, including Department of Defense employees and contractors. This overlap allows NFCU members to join USAA if they qualify, enabling them to leverage the unique benefits of both institutions.

When comparing Navy Federal vs. USAA benefits, one notable difference lies in their financial products. NFCU excels in banking services, offering competitive rates on savings accounts, low-interest loans, and no-fee checking accounts. For instance, their Certificate of Deposit (CD) rates often outperform national averages, making it an attractive option for long-term savings. USAA, on the other hand, stands out in insurance and investment services. Their auto and homeowners insurance policies are highly rated for affordability and coverage, with discounts for safe driving and bundling. Additionally, USAA’s investment management tools, including retirement accounts and mutual funds, provide comprehensive financial planning options. To maximize benefits, consider using NFCU for daily banking and USAA for insurance and investments.

Another critical comparison is customer service and accessibility. NFCU operates a vast network of branches and ATMs, particularly near military bases, making it convenient for active-duty members. Their 24/7 customer service and user-friendly mobile app enhance accessibility. USAA, while lacking physical branches, compensates with exceptional phone and online support, including dedicated representatives for specific financial needs. For example, USAA offers specialized assistance for deployment-related financial planning, a feature particularly valuable for military families. Both institutions prioritize security, with NFCU offering free credit monitoring and USAA providing identity theft protection as part of their insurance packages.

For those eligible for both, combining NFCU and USAA memberships can create a robust financial strategy. Start by opening a checking and savings account with NFCU to take advantage of their fee-free structure and high-interest savings options. Simultaneously, secure auto and homeowners insurance through USAA to benefit from their competitive rates and military-specific discounts. If you’re planning for retirement, USAA’s investment advisors can help tailor a portfolio to your goals. Caution: Avoid duplicating services; for instance, if you have NFCU’s credit monitoring, you may not need USAA’s identity theft protection unless it’s bundled at no extra cost. By strategically utilizing both institutions, you can optimize financial stability and growth.

In conclusion, while NFCU and USAA serve similar demographics, their benefits are complementary rather than redundant. NFCU’s strength lies in banking services, while USAA excels in insurance and investments. Eligibility for both allows members to create a diversified financial portfolio tailored to their needs. Practical steps include assessing your financial priorities, comparing specific product offerings, and leveraging the unique advantages of each institution. For example, a young service member might prioritize NFCU’s low-interest car loans and USAA’s affordable renters insurance. By understanding the nuances of Navy Federal vs. USAA benefits, you can make informed decisions to enhance your financial well-being.

Navy Stationing Explained: Where Will Your Service Take You?

You may want to see also

Explore related products

$43.34 $47.78

![]()

Cross-Membership Possibilities

Membership in financial institutions often comes with specific eligibility requirements, but savvy consumers frequently explore cross-membership possibilities to maximize benefits. For instance, Navy Federal Credit Union (NFCU) members often wonder if they can also join USAA, a financial services group known for its military-focused offerings. The key lies in understanding the distinct eligibility criteria of each organization. NFCU requires a direct connection to the military or Department of Defense, while USAA extends membership to military personnel, veterans, and their families. This overlap creates a unique opportunity for cross-membership, allowing individuals to access the benefits of both institutions simultaneously.

To pursue cross-membership, start by verifying your eligibility for both NFCU and USAA. If you’re active-duty military, a veteran, or a family member of someone who serves, you likely qualify for USAA. Once confirmed, apply for USAA membership online or via phone, providing necessary documentation such as military records or dependent verification. Importantly, maintaining NFCU membership does not disqualify you from joining USAA, as the two organizations operate independently. This dual membership can be particularly advantageous, as NFCU offers competitive loan rates and robust savings accounts, while USAA provides comprehensive insurance and investment products.

A practical tip for maximizing cross-membership benefits is to allocate services strategically. For example, use NFCU for primary banking needs like checking and savings accounts, while leveraging USAA for auto and home insurance, where they often offer superior rates and coverage. Additionally, consider USAA’s investment tools for long-term financial planning, complementing NFCU’s short-term financial products. This approach ensures you capitalize on the strengths of both institutions without redundancy.

However, be mindful of potential pitfalls. While cross-membership is feasible, managing multiple accounts requires organization. Use budgeting apps or spreadsheets to track transactions and avoid overlapping services that could lead to unnecessary fees. Also, stay informed about changes in eligibility or benefits, as both organizations periodically update their offerings. By staying proactive and strategic, you can seamlessly integrate NFCU and USAA memberships to build a comprehensive financial portfolio tailored to your needs.

Navy Payday Schedule: Understanding When Sailors Receive Their Earnings

You may want to see also

Explore related products

![]()

Application Process for USAA

Membership in Navy Federal Credit Union (NFCU) does not automatically qualify someone for USAA membership, but it can be a stepping stone. USAA, historically exclusive to military members and their families, has expanded its eligibility criteria. If you’re a NFCU member, chances are you have a military affiliation, which is a key requirement for USAA. However, simply being part of NFCU isn’t enough—you must meet USAA’s specific eligibility rules, such as being an active-duty service member, veteran, or eligible family member.

The application process for USAA begins with verifying your eligibility. Visit USAA’s website and navigate to their membership application page. You’ll be prompted to provide personal information, including your military status, branch of service, and dates of service. If you’re a veteran, have your DD-214 or other discharge documents ready. For eligible family members, proof of relationship to a USAA member (e.g., marriage certificate or birth certificate) is required. Accuracy is critical here—errors can delay approval.

Once eligibility is confirmed, the next step is to choose the products or services you’re interested in. USAA offers banking, insurance, investments, and retirement planning. Unlike NFCU, which focuses primarily on financial services, USAA provides a broader range of offerings tailored to military life. For instance, their auto insurance includes features like coverage for uniforms and moving vehicle expenses, which are unique to military needs. Selecting the right products during the application process ensures you maximize the benefits of membership.

After submitting your application, USAA typically processes it within a few business days. If approved, you’ll receive a welcome packet with details on how to access your account and services. One practical tip: link your NFCU account to your new USAA account for seamless transfers. While NFCU and USAA both cater to military communities, USAA’s additional services, like deployment discounts and specialized financial advice, make it a valuable complement to your existing NFCU membership.

In summary, while NFCU membership doesn’t guarantee USAA eligibility, your military affiliation likely does. The application process is straightforward but requires specific documentation. By leveraging both institutions, you can access a comprehensive suite of financial and insurance services tailored to military life.

Travel Time to Chicago: Factors Affecting Your Journey Duration

You may want to see also

Explore related products

![]()

Shared Services and Limitations

Membership in Navy Federal Credit Union (NFCU) and USAA often overlaps due to their shared focus on serving military communities, but their services and eligibility criteria differ significantly. While both institutions offer financial products tailored to military personnel and their families, they operate under distinct models. NFCU is a credit union, requiring membership based on military affiliation, employment, or family ties. USAA, on the other hand, is a privately held financial services company with membership traditionally limited to active military, veterans, and their immediate families. This fundamental difference in structure creates a natural boundary for shared services, as each institution maintains its own set of offerings and eligibility rules.

One area where shared services emerge is in partnerships and co-branded offerings. For instance, NFCU and USAA may collaborate on insurance products or investment services, leveraging their combined expertise to benefit members. However, these partnerships are limited in scope and do not grant NFCU members automatic access to USAA’s full suite of services, such as its renowned banking or insurance products. Members must independently qualify for USAA by meeting its eligibility criteria, which includes providing proof of military affiliation. This limitation underscores the importance of understanding the distinct identities of these institutions, even when they collaborate.

A practical example of this limitation is the inability of an NFCU member to access USAA’s auto or home insurance policies without first becoming a USAA member. While both institutions may offer competitive rates, the application processes and eligibility requirements remain separate. For instance, a Navy Federal member seeking USAA insurance must first verify their military status through USAA’s system, often requiring documentation like a DD Form 214 or military orders. This process highlights the operational independence of the two entities, despite their shared target audience.

To navigate these limitations, individuals should focus on maximizing the benefits of their existing memberships while exploring eligibility for additional services. For example, NFCU members can take advantage of the credit union’s low-interest loans and robust savings accounts, while simultaneously applying for USAA membership to access its specialized insurance and investment products. A step-by-step approach includes: verifying military eligibility for USAA, gathering necessary documentation, and submitting an application directly through USAA’s website. Caution should be exercised to avoid assuming automatic cross-membership, as this is not the case.

In conclusion, while Navy Federal Credit Union and USAA share a focus on serving military communities, their services and eligibility criteria remain distinct. Shared offerings are limited to specific partnerships, and members must independently qualify for each institution’s benefits. By understanding these limitations and taking proactive steps to meet eligibility requirements, individuals can strategically leverage the strengths of both NFCU and USAA to meet their financial needs.

The Surprising Origin Story of Navy Beans' Name Revealed

You may want to see also

Frequently asked questions

Yes, a member of Navy Federal Credit Union can also join USAA, as the two organizations are separate and have different eligibility requirements.

While both offer financial services like banking, loans, and insurance, they are distinct entities with unique products and eligibility criteria.

Yes, individuals who qualify for NFCU (e.g., military members, veterans, and their families) often also meet USAA’s eligibility requirements, which include active military, veterans, and their families.

Yes, you can use both services simultaneously, as they are independent organizations and do not restrict members from using other financial institutions.

The choice depends on individual needs. NFCU is primarily a credit union offering banking and loans, while USAA provides insurance, banking, and investment services. Compare their offerings to decide which suits you best.