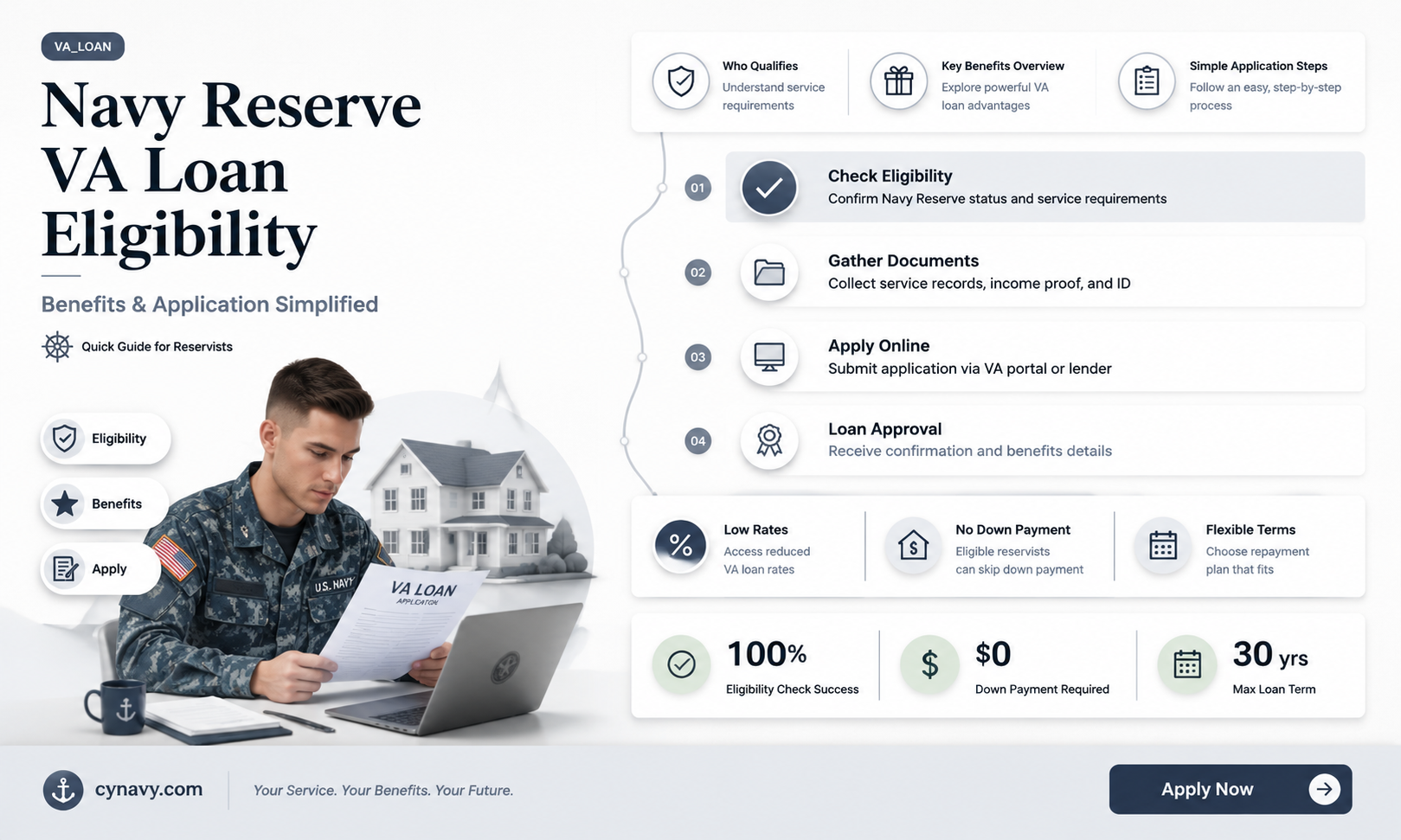

For individuals considering joining the Navy Reserve or those already serving, understanding the benefits available, such as a VA loan, is crucial. A VA loan is a mortgage option backed by the Department of Veterans Affairs, offering favorable terms like no down payment and no private mortgage insurance. Many Navy Reserve members wonder if they qualify for this benefit, as it can significantly ease the process of homeownership. Eligibility for a VA loan typically requires a certain period of service, and Navy Reserve members can indeed qualify, provided they meet specific criteria, including the length of service and honorable discharge status. This benefit extends to reservists who have completed the necessary training and active duty requirements, making it an attractive financial tool for those committed to serving their country in a part-time capacity.

| Characteristics | Values |

|---|---|

| Eligibility for VA Loan | Navy Reserves are eligible for VA loans after meeting service requirements. |

| Minimum Service Requirement | 6 years in the Selected Reserve or National Guard, with certain exceptions. |

| Exceptions to Service Requirement | 90 consecutive days of active service during wartime or 181 days during peacetime. |

| Discharge Status | Honorable or other than dishonorable discharge required. |

| Funding Fee | Applies, but may be waived for service-connected disabilities. |

| Loan Limits | No maximum loan limit, but VA guarantees up to $726,200 (2023) in high-cost areas. |

| Credit Requirements | No minimum credit score set by VA, but lenders may have their own criteria. |

| Income Verification | Stable, reliable income required to qualify. |

| Property Requirements | Must be a primary residence; VA appraisal required. |

| Reusable Benefit | Can use VA loan benefit multiple times after paying off previous loans. |

| Surviving Spouse Eligibility | Surviving spouses of Navy Reservists may also be eligible under certain conditions. |

| Certificate of Eligibility (COE) | Required to prove eligibility to lenders. |

| Application Process | Apply through a VA-approved lender; COE can be obtained online or via mail. |

| Benefits | No down payment, no PMI, competitive interest rates, and flexible terms. |

Explore related products

What You'll Learn

- Eligibility requirements for Navy Reserves to qualify for a VA loan

- Minimum service time needed for VA loan benefits in the Reserves

- Required documentation for Navy Reserves applying for a VA loan

- Differences between active duty and Reserve VA loan entitlements

- How to obtain a Certificate of Eligibility (COE) as a Reservist?

![]()

Eligibility requirements for Navy Reserves to qualify for a VA loan

Navy Reserves members seeking a VA loan must meet specific service requirements to qualify for this valuable benefit. Unlike active-duty personnel, reservists face a longer minimum service period: six years in the Selected Reserve or National Guard, with at least 90 consecutive days of active service during wartime or six years of honorable service with a combination of active and inactive duty points. This distinction highlights the VA’s tiered approach to eligibility, ensuring benefits align with service commitment.

To initiate the VA loan process, Navy Reserves must obtain a Certificate of Eligibility (COE), which verifies their service meets VA standards. This document can be acquired through the VA’s eBenefits portal, a lender using WebLGY, or by submitting VA Form 26-1880 with supporting military records. Reservists should ensure their NGB Form 23 (Retirement Points Accounting) or a statement of service from their unit commander is included, as these documents provide critical proof of qualifying service.

One common challenge for Navy Reserves is meeting the active duty requirement, particularly the 90-day minimum during wartime. However, reservists called to active duty for training or in support of a federal mission may count these periods toward eligibility. For example, service during Operations Enduring Freedom or Iraqi Freedom qualifies, even if the reservist was not deployed overseas. Understanding these nuances can help reservists accurately assess their eligibility and avoid unnecessary delays.

Finally, while the VA loan program offers significant advantages, such as no down payment or private mortgage insurance, Navy Reserves should be aware of the funding fee—a one-time payment that varies based on service category and down payment amount. First-time users pay 2.15% of the loan amount, while subsequent users pay 3.3%. Reservists can reduce this fee by making a down payment of at least 5%, making it a strategic consideration when planning their home purchase. By carefully navigating these eligibility requirements, Navy Reserves can leverage the VA loan program to achieve homeownership with favorable terms.

Accessing Voided Checks via Navy Federal App: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Minimum service time needed for VA loan benefits in the Reserves

Navy Reserves members seeking VA loan benefits must meet specific service time requirements, which are distinct from those for active-duty personnel. The Department of Veterans Affairs (VA) mandates that Reserves and National Guard members complete a minimum of six years of honorable service to qualify for a VA loan. However, there’s an important exception: if a Reserve member is called to active duty for 90 consecutive days or more, the minimum service time is reduced. This flexibility acknowledges the unique contributions of part-time service members while ensuring eligibility criteria are met.

To break it down further, Reserves members who have not been activated must serve at least six years in a selected reserve unit, with satisfactory participation, to become eligible. This includes attending required drills and training sessions. For those who are activated, the 90-day active-duty requirement opens the door to VA loan benefits much sooner, provided the service is honorable. It’s crucial to document this service accurately, as the VA will verify eligibility through the Department of Defense.

A practical tip for Reserves members is to keep detailed records of their service, including drill attendance, training periods, and any activation orders. This documentation can streamline the VA loan application process and prevent delays. Additionally, Reserves members should be aware that the six-year requirement can be fulfilled through a combination of active duty and reserve service, offering another pathway to eligibility. Understanding these nuances ensures that part-time service members can maximize their benefits effectively.

Comparatively, active-duty members typically qualify for VA loan benefits after just 90 consecutive days of service, highlighting the longer commitment required of Reserves. However, the Reserves’ eligibility criteria are designed to recognize the cumulative dedication of part-time service. For those nearing the six-year mark, planning ahead—such as ensuring consistent drill attendance—can make the difference in securing VA loan eligibility. This structured approach ensures Reserves members are well-prepared to leverage this valuable benefit.

In conclusion, while the minimum service time for Reserves members to qualify for a VA loan is six years, exceptions and combinations of service can expedite eligibility. By understanding these requirements and maintaining thorough records, Navy Reserves members can confidently pursue VA loan benefits as a reward for their service. This tailored approach ensures that part-time service members are not overlooked in accessing the financial support they’ve earned.

Does Navy Federal Offer Early Paycheck Deposits? Find Out Here

You may want to see also

Explore related products

![]()

Required documentation for Navy Reserves applying for a VA loan

Navy Reserves seeking a VA loan must provide specific documentation to verify their eligibility and service status. The cornerstone of this process is the Certificate of Eligibility (COE), which confirms to lenders that you meet the VA’s service requirements. To obtain the COE, Navy Reserves typically need to submit a copy of their DD Form 214 if they have prior active duty service, or their Statement of Service signed by their commanding officer if they are currently serving. This statement must include your full name, Social Security number, date of birth, entry date into the Navy Reserves, and total number of creditable years of service.

Beyond the COE, lenders will require additional documentation to assess your financial readiness. This includes proof of income, such as recent pay stubs or tax returns, to demonstrate your ability to repay the loan. Bank statements and asset documentation are also essential to verify your financial stability and reserves. For Navy Reserves, it’s crucial to ensure all service-related documents are up-to-date, as gaps in service records can delay the approval process. If you’ve had breaks in service, provide a detailed explanation to avoid misunderstandings.

One often-overlooked document is the NGB Form 23 (for Army and Air National Guard members) or its Navy equivalent, which outlines your retirement points and years of service. While not always required, this form can strengthen your application by providing a comprehensive view of your military commitment. Additionally, if you’ve served under Title 32 or Title 10 orders, include documentation of these periods, as they may count toward your eligibility.

Finally, be prepared for lenders to request credit reports and employment verification. While these are standard for all loan applications, Navy Reserves should ensure their credit history is in good standing, as the VA loan program does not have a minimum credit score requirement, but lenders often do. Keep all documents organized and readily accessible to streamline the process. By proactively gathering these materials, Navy Reserves can navigate the VA loan application with confidence and efficiency.

Understanding ACH Credits: Why Navy Federal Deposited Funds in Your Account

You may want to see also

Explore related products

![]()

Differences between active duty and Reserve VA loan entitlements

Navy Reserves, like their active-duty counterparts, are eligible for VA loans, but the path to securing this benefit differs significantly. Active-duty members typically qualify after 90 consecutive days of service during wartime or 181 days during peacetime. Reserves, however, must complete six years of selected reserve service or a combination of reserve and active duty totaling six years to meet the eligibility threshold. This extended timeline reflects the part-time nature of reserve service but ensures that reservists can still access this valuable benefit.

One critical difference lies in the Certificate of Eligibility (COE), a document required to apply for a VA loan. Active-duty members can often obtain their COE through their chain of command or online via the eBenefits portal. Reserves, on the other hand, must typically request their COE directly from the VA, which can involve additional paperwork and processing time. This process underscores the importance of planning ahead for reservists seeking to use their VA loan entitlement.

Another distinction is the funding fee, a one-time payment that helps offset the cost of the VA loan program. For first-time users, active-duty members pay 2.15% of the loan amount, while Reserves pay 2.4%. Subsequent use of the VA loan benefit increases the funding fee for both groups, but Reserves face a slightly higher rate. However, certain exemptions apply, such as for service-connected disabilities, which can waive the funding fee entirely.

Practical considerations also come into play when comparing loan limits. Both active-duty and Reserve members have access to the VA’s no-down-payment benefit, but the loan limit without a down payment varies by county. In high-cost areas, Reserves may need to make a down payment if the loan exceeds the VA’s conforming limit, whereas active-duty members might have more flexibility due to higher income levels. Understanding these nuances can help reservists navigate the homebuying process more effectively.

Finally, the continuity of service requirement is more stringent for Reserves. Active-duty members have a clear timeline for eligibility, but Reserves must maintain satisfactory service without extended breaks. A gap in service exceeding 90 days may require a reevaluation of eligibility, adding complexity to the process. Reservists should keep detailed records of their service history to streamline the VA loan application and ensure they meet all criteria.

Secure Your Army-Navy Game Tickets: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How to obtain a Certificate of Eligibility (COE) as a Reservist

Navy Reservists, like their active-duty counterparts, are eligible for VA home loans, a benefit that can significantly ease the path to homeownership. However, the first step in this process is obtaining a Certificate of Eligibility (COE), a document that proves to lenders you meet the VA’s service requirements. For Reservists, this process involves specific criteria and documentation that differ slightly from active-duty personnel. Here’s how to navigate it effectively.

Step 1: Verify Your Service Requirements

As a Reservist, you must meet one of the following criteria to qualify for a COE: at least six years of service in the Selected Reserve or National Guard, completion of the initial active-duty training period, or discharge due to a service-connected disability. If you’ve been activated and served on active duty, the requirements may be reduced. For example, 90 consecutive days of active service during wartime or 181 days during peacetime can qualify you. Ensure your service records reflect these milestones accurately.

Step 2: Gather Required Documentation

To apply for a COE, you’ll need specific documents. These typically include a copy of your latest orders, a statement of service signed by your commanding officer, or a Report of Separation (DD Form 214) if you’ve been discharged. If you’re still serving, your unit administrator can provide a signed statement verifying your service dates and character of service. Double-check that all documents are up-to-date and clearly state your service period and status.

Step 3: Apply for Your COE

There are three primary ways to apply for a COE: online through the VA’s eBenefits portal, by mail using VA Form 26-1880, or through your lender, who can often obtain it on your behalf via the VA’s WebLGY system. The online method is the fastest, typically providing instant approval if your service records are in the VA’s system. If you encounter delays, contact the VA’s regional loan center for assistance.

Cautions and Practical Tips

Be aware that incomplete applications or discrepancies in service records can delay the process. If your service history isn’t automatically verified, you may need to provide additional documentation. Keep copies of all submitted materials and follow up regularly. Additionally, if you’ve transferred from active duty to the Reserves, ensure your records reflect both service periods. Finally, while the COE doesn’t expire, your lender may require an updated version if your financial situation changes significantly.

Obtaining a COE as a Reservist is a straightforward process if you understand the requirements and prepare the necessary documentation. By verifying your service, gathering the right paperwork, and choosing the most efficient application method, you can secure this critical document and move forward with your VA home loan application. This step not only unlocks access to favorable loan terms but also honors your commitment to service by providing a pathway to homeownership.

Can You Secure a Loan from Navy Federal? A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, Navy Reserve members can qualify for a VA loan after completing the required service period, typically six years in the Selected Reserve or National Guard, or earlier if discharged due to a service-related disability.

Navy Reserve members must serve at least six years in the Selected Reserve or National Guard. Alternatively, they may qualify earlier if they are discharged due to a service-connected disability, complete 90 consecutive days of active service during wartime, or 181 consecutive days during peacetime.

Yes, Navy Reserve members must obtain a Certificate of Eligibility (COE) to prove their eligibility for a VA loan. This can be requested online through the VA’s eBenefits portal, by mail, or through a VA-approved lender.