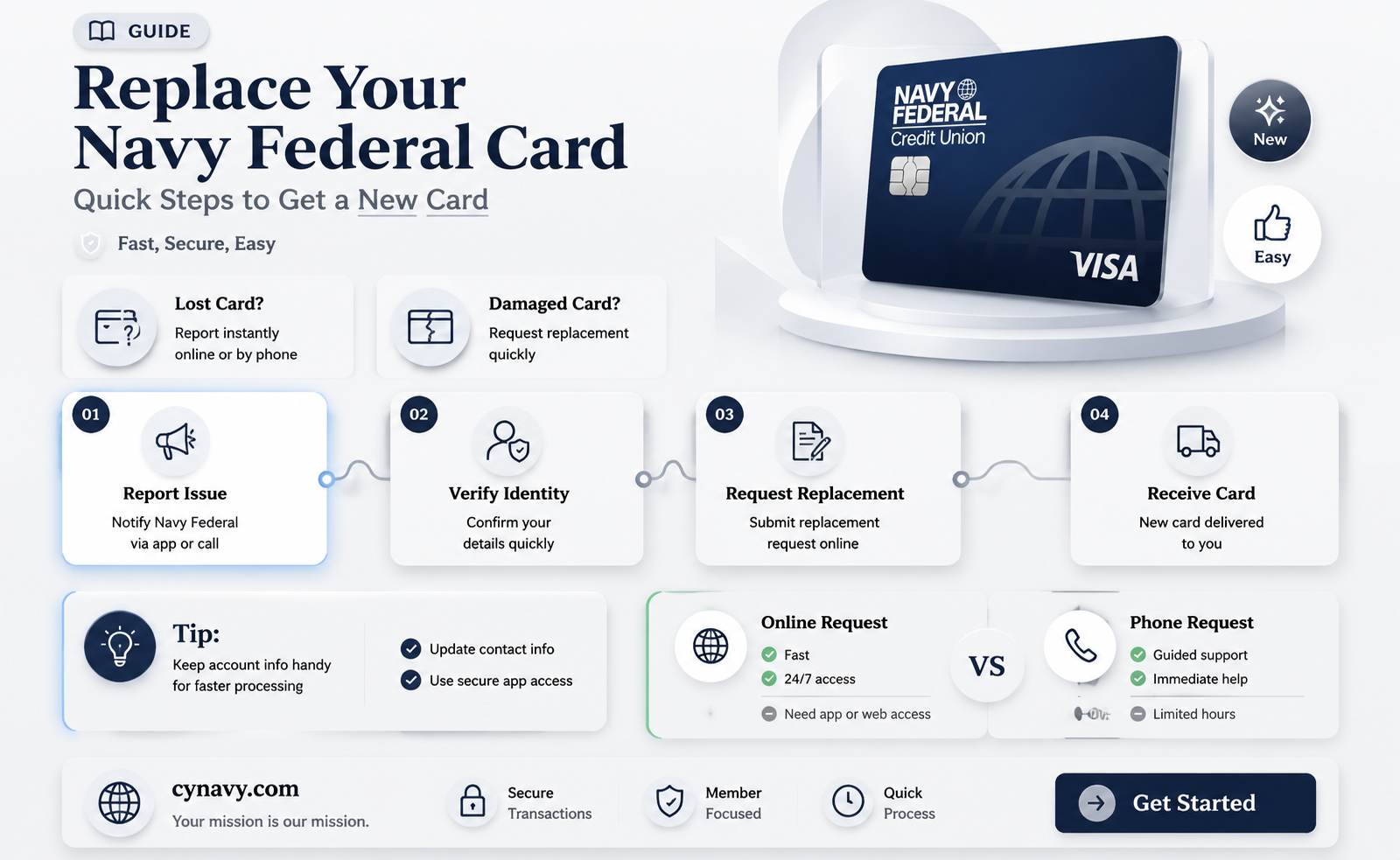

If you're a Navy Federal Credit Union member and need a new card, whether due to loss, theft, damage, or expiration, the process is straightforward. Navy Federal offers several options to request a replacement card, including online through their secure portal, via their mobile app, or by contacting their customer service team. Members can typically expect to receive their new card within 7-10 business days, though expedited shipping may be available for an additional fee. It’s important to report a lost or stolen card immediately to prevent unauthorized use and ensure your account remains secure. Additionally, Navy Federal may provide temporary solutions, such as digital wallet access, while you wait for your physical card to arrive.

| Characteristics | Values |

|---|---|

| Eligibility | Must be a Navy Federal Credit Union member. |

| Membership Requirements | Active Duty or Retired Military, Veterans, Department of Defense civilians, family members of existing members. |

| Application Process | Online, via phone, or in-person at a branch. |

| Types of Cards Available | Credit cards (e.g., cashRewards, More Rewards, Flagship Rewards), Debit cards, Prepaid cards. |

| Replacement Card Fee | Typically free for lost, stolen, or damaged cards. |

| Expedited Card Delivery | Available for a fee (usually $25-$30). |

| Card Activation | Required after receipt; can be done online or via phone. |

| Credit Limit | Varies based on creditworthiness and income. |

| APR (Annual Percentage Rate) | Competitive rates, starting as low as 7.99% (varies by card type). |

| Rewards Program | Available on select cards (e.g., cash back, points for travel). |

| Fraud Protection | 24/7 monitoring and zero liability for unauthorized charges. |

| International Use | Cards can be used globally with no foreign transaction fees on some cards. |

| Customer Support | 24/7 customer service via phone, chat, or email. |

| Mobile App Integration | Manage card, track spending, and make payments via the Navy Federal app. |

| Additional Benefits | Rental car insurance, extended warranty, and travel assistance on select cards. |

| Credit Reporting | Reports to all three major credit bureaus (Equifax, Experian, TransUnion). |

| Annual Fee | Varies by card; some cards have no annual fee. |

Explore related products

What You'll Learn

- Eligibility Requirements: Check income, credit score, and membership status to qualify for a new Navy Federal card

- Application Process: Apply online, by phone, or in-branch with required documents and personal details

- Card Options: Explore credit, debit, or secured cards tailored to your financial needs

- Fees & Rates: Review annual fees, APRs, and other charges associated with the card

- Activation Steps: Activate your new card via Navy Federal’s website, app, or phone service

![]()

Eligibility Requirements: Check income, credit score, and membership status to qualify for a new Navy Federal card

To qualify for a new Navy Federal card, understanding the eligibility requirements is crucial. These requirements are designed to ensure that applicants meet certain financial and membership criteria, reflecting the credit union’s commitment to responsible lending and member-focused services. Let’s break down the key factors: income, credit score, and membership status.

Income Verification: The Foundation of Financial Stability

Navy Federal evaluates your income to assess your ability to manage credit responsibly. While there’s no strict minimum income threshold, a consistent and sufficient income stream is essential. For example, applicants with annual incomes above $30,000 may have a stronger case, but this isn’t a hard rule. The credit union considers your debt-to-income ratio (DTI), ideally below 40%, to gauge affordability. Pro tip: Gather recent pay stubs, tax returns, or bank statements to streamline the verification process.

Credit Score: The Gateway to Approval

Your credit score plays a pivotal role in determining eligibility. Navy Federal typically favors applicants with scores of 660 or higher for most cards, though some premium options may require scores above 700. For instance, the Navy Federal Flagship Rewards card often targets individuals with excellent credit (750+). If your score is below 660, consider secured cards like the Navy Federal nRewards Secured, which requires a refundable deposit but helps build credit. Practical advice: Check your credit report for errors and address them before applying to maximize your chances.

Membership Status: The Non-Negotiable Requirement

Unlike traditional banks, Navy Federal is a credit union with specific membership criteria. Eligibility extends to active-duty military, veterans, Department of Defense employees, and their families. If you’re not directly affiliated, you may qualify through a family member or by joining a military-affiliated organization like the Navy League. Without membership, you cannot apply for a Navy Federal card. Key takeaway: Verify your eligibility through their online tool or by contacting customer service before proceeding.

Combining Factors for Success

Meeting one eligibility requirement isn’t enough; Navy Federal evaluates your application holistically. For example, a high income and excellent credit score won’t compensate for non-membership. Conversely, a strong membership status paired with a fair credit score and stable income could still lead to approval. Comparative analysis: While other institutions may prioritize credit scores above all, Navy Federal balances financial health with community affiliation, reflecting its mission to serve military families.

Practical Steps to Enhance Eligibility

If you’re on the cusp of qualifying, take proactive steps. Increase your credit score by paying bills on time and reducing debt. Boost your income stability by avoiding frequent job changes. If you’re not yet a member, explore eligibility pathways immediately. Final tip: Apply for a card that aligns with your financial profile—starting with a secured card or lower-tier rewards card can build trust for future upgrades. By addressing these requirements strategically, you’ll position yourself for success in obtaining a new Navy Federal card.

Steps to Join Navy Federal Credit Union: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Application Process: Apply online, by phone, or in-branch with required documents and personal details

Applying for a new card at Navy Federal Credit Union is a straightforward process, offering multiple channels to suit your preference: online, by phone, or in-branch. Each method requires specific documents and personal details, ensuring a secure and efficient application. Let’s break down the steps and considerations for each approach.

Online Application: Convenience at Your Fingertips

The online application is the most popular choice for its speed and accessibility. Start by logging into your Navy Federal account or creating one if you’re a new member. Navigate to the credit card section, select your desired card, and fill out the application form. Required documents typically include proof of identity (e.g., driver’s license, passport), Social Security number, and income verification. Pro tip: Have your documents scanned or photographed in advance to streamline the process. The online system often provides instant pre-approval decisions, making it ideal for those seeking quick feedback.

Phone Application: Personalized Assistance

If you prefer human interaction or need guidance, applying by phone is a solid option. Call Navy Federal’s customer service line and follow the prompts to reach a representative specializing in card applications. They’ll guide you through the process, answer questions, and verify your details. Be prepared to provide the same documents as the online method, though you may need to fax or email them afterward. This method is particularly useful for older adults or those less comfortable with digital platforms. Note that phone applications may take slightly longer due to the back-and-forth communication.

In-Branch Application: Face-to-Face Reliability

For a hands-on experience, visiting a Navy Federal branch allows you to apply in person with the assistance of a financial representative. Bring all required documents, including government-issued ID, proof of income, and Social Security number verification. The representative will review your application, address any concerns, and submit it on your behalf. This method is ideal for complex financial situations or if you prefer tangible interactions. However, it requires scheduling and travel, so plan accordingly.

Key Takeaways: Choose What Works Best for You

Each application method has its advantages. Online is fastest, phone offers personalized help, and in-branch provides face-to-face assurance. Regardless of your choice, ensure your documents are ready and your personal details are accurate to avoid delays. Navy Federal’s multi-channel approach ensures accessibility, so you can select the process that aligns with your comfort and needs.

How to Easily Obtain a Checkbook from Navy Federal Credit Union

You may want to see also

Explore related products

![]()

Card Options: Explore credit, debit, or secured cards tailored to your financial needs

Navy Federal Credit Union offers a diverse range of card options designed to meet the unique financial needs of its members. Whether you're looking to build credit, manage spending, or earn rewards, understanding the differences between credit, debit, and secured cards is crucial. Each type serves distinct purposes, and choosing the right one can significantly impact your financial health.

Credit Cards: Flexibility and Rewards

Navy Federal’s credit cards are ideal for members seeking flexibility and rewards. Options like the Navy Federal More Rewards American Express Card offer up to 3x points on everyday purchases, while the cashRewards card provides 1.75% cashback on all transactions. These cards are best for those with established credit who can manage monthly payments responsibly. A key advantage is the ability to build credit history through consistent, on-time payments. However, high interest rates on unpaid balances can offset rewards if not managed carefully. For maximum benefit, pay off the balance in full each month to avoid accruing interest.

Debit Cards: Simplicity and Control

For members prioritizing simplicity and spending control, Navy Federal’s debit cards are a straightforward choice. Linked directly to your checking account, these cards allow you to spend only what you have, eliminating the risk of debt. They’re particularly useful for budgeting or for those who prefer not to use credit. While debit cards don’t offer the same rewards as credit cards, some Navy Federal options include perks like cashback on certain purchases or ATM fee rebates. This makes them a practical tool for everyday transactions without the complexity of credit management.

Secured Cards: Building or Rebuilding Credit

If your credit score is low or nonexistent, Navy Federal’s secured credit cards provide a pathway to improvement. These cards require a security deposit, typically ranging from $200 to $3,000, which becomes your credit limit. Responsible use—such as keeping balances low and making timely payments—can help establish or repair credit history. Unlike unsecured cards, secured options are more accessible to those with limited or poor credit. Over time, consistent positive behavior may allow you to upgrade to an unsecured card and get your deposit back. This makes secured cards a strategic choice for long-term financial growth.

Choosing the Right Card: Practical Tips

To select the best card, assess your financial goals and habits. If you’re disciplined with spending and want to maximize rewards, a credit card could be ideal. For those who prefer debt-free spending, a debit card offers peace of mind. Secured cards are the go-to for credit-building or recovery. Consider factors like annual fees, interest rates, and rewards structures. Navy Federal also provides tools like credit score monitoring and financial education resources to help members make informed decisions. By aligning your choice with your needs, you can leverage these cards to achieve financial stability and growth.

Unlocking Navy Federal Credit Union Membership: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Fees & Rates: Review annual fees, APRs, and other charges associated with the card

Before committing to a new credit card from Navy Federal, scrutinize the annual fees, APRs, and additional charges to ensure the card aligns with your financial goals. Annual fees can range from $0 to $150 or more, depending on the card’s rewards and benefits. For instance, the Navy Federal More Rewards American Express Card carries no annual fee, making it an attractive option for those who prioritize cost savings. In contrast, premium cards like the Navy Federal Flagship Rewards Card charge an annual fee but offer higher rewards rates and travel perks. Evaluate whether the benefits outweigh the cost before applying.

APR (Annual Percentage Rate) is another critical factor, as it determines the cost of carrying a balance. Navy Federal’s credit cards typically offer variable APRs ranging from 7.99% to 18.00%, depending on your creditworthiness and the card type. For example, the Navy Federal cashRewards Credit Card may offer a lower APR for members with excellent credit, while secured cards might have slightly higher rates. If you plan to carry a balance, prioritize cards with lower APRs to minimize interest expenses. Remember, promotional APRs for balance transfers or purchases often expire after 6–18 months, so review the terms carefully.

Beyond annual fees and APRs, additional charges can add up quickly if overlooked. Navy Federal cards generally waive foreign transaction fees, making them ideal for international travelers. However, other fees like balance transfer fees (typically 3% of the amount transferred), cash advance fees (up to 2% of the advance), and late payment fees (up to $20) apply. For instance, if you transfer a $5,000 balance, a 3% fee would cost you $150 upfront. To avoid unnecessary charges, set up autopay for at least the minimum due and use the card responsibly.

A comparative analysis of Navy Federal’s cards reveals that while some offer lower fees, others provide greater value through rewards. For example, the Navy Federal More Rewards Card has no annual fee and earns 3x points on travel and dining, but its APR might be higher than the cashRewards Card, which offers 1.75% cashback with a potentially lower APR. If you’re a frequent traveler, the Flagship Rewards Card’s $49 annual fee could be justified by its 3x points on travel and $100 annual travel credit. Weigh your spending habits against the card’s fees and rewards to determine the best fit.

Finally, practical tips can help you maximize value while minimizing costs. If you’re unsure about a card’s fees, contact Navy Federal’s customer service for clarification. Consider pairing a no-annual-fee card with a premium card to balance costs and benefits. For instance, use the More Rewards Card for everyday spending and the Flagship Card for travel to leverage both rewards structures. Additionally, pay your balance in full each month to avoid APR charges altogether. By carefully reviewing fees and rates, you can select a Navy Federal card that enhances your financial strategy without hidden surprises.

Navy Flyover for a Birthday: Is It Possible and How?

You may want to see also

Explore related products

![]()

Activation Steps: Activate your new card via Navy Federal’s website, app, or phone service

Receiving a new card from Navy Federal is just the first step; activating it is crucial to unlock its full potential. Activation ensures your card is secure and ready for use, whether you're making purchases, accessing funds, or managing your account. Navy Federal offers multiple convenient methods to activate your card, catering to different preferences and needs. Whether you're tech-savvy or prefer traditional methods, the process is designed to be straightforward and user-friendly.

Step-by-Step Activation via Website:

Log in to your Navy Federal account on their official website using your credentials. Navigate to the "Credit/Debit Cards" section, where you’ll find an option to activate your new card. Enter the required details, such as the card number and expiration date, and follow the prompts to complete the activation. This method is ideal for those who prefer a desktop experience and want to verify their card details in detail. Ensure you’re using a secure browser and connection to protect your information.

Activation Through the Mobile App:

For on-the-go convenience, Navy Federal’s mobile app provides a seamless activation process. Download the app if you haven’t already, and log in with your account details. Locate the card management section, select your new card, and follow the instructions to activate it. The app often includes additional features like setting up transaction alerts or locking your card temporarily, giving you greater control over your finances. This method is perfect for users who prioritize accessibility and quick actions.

Phone Activation for Personal Assistance:

If you prefer a more personal touch or need assistance, Navy Federal’s phone service is a reliable option. Call the number provided on the sticker attached to your new card or on the back of the card itself. Follow the automated prompts or speak to a representative to complete the activation. This method is particularly useful for those who may have questions or concerns during the process. Be prepared to provide verification details, such as your Social Security number or account information, for security purposes.

Cautions and Tips:

Regardless of the method you choose, ensure your card information remains confidential. Avoid activating your card on public Wi-Fi networks or sharing details with unauthorized individuals. If you encounter issues during activation, such as incorrect card details or system errors, contact Navy Federal’s customer service immediately. Once activated, sign the back of your card and consider setting up digital wallet options for added convenience. Remember, activation is the final step before your card is fully functional, so proceed with care and attention to detail.

Can Civilians Join Navy Federal Credit Union? Eligibility Explained

You may want to see also

Frequently asked questions

Yes, you can request a replacement card immediately by logging into your Navy Federal account online, using the mobile app, or calling their customer service at 1-888-842-6328.

Typically, it takes 7-10 business days to receive a new card after requesting it, though expedited shipping options may be available for an additional fee.

Navy Federal generally does not charge a fee for replacing a lost, stolen, or damaged card, but expedited delivery may incur a cost.

Yes, Navy Federal offers various card designs, and you can choose a new one when requesting a replacement, depending on availability.

Navy Federal typically sends a replacement card automatically before your current one expires. If you haven’t received it, contact customer service to request a new card.