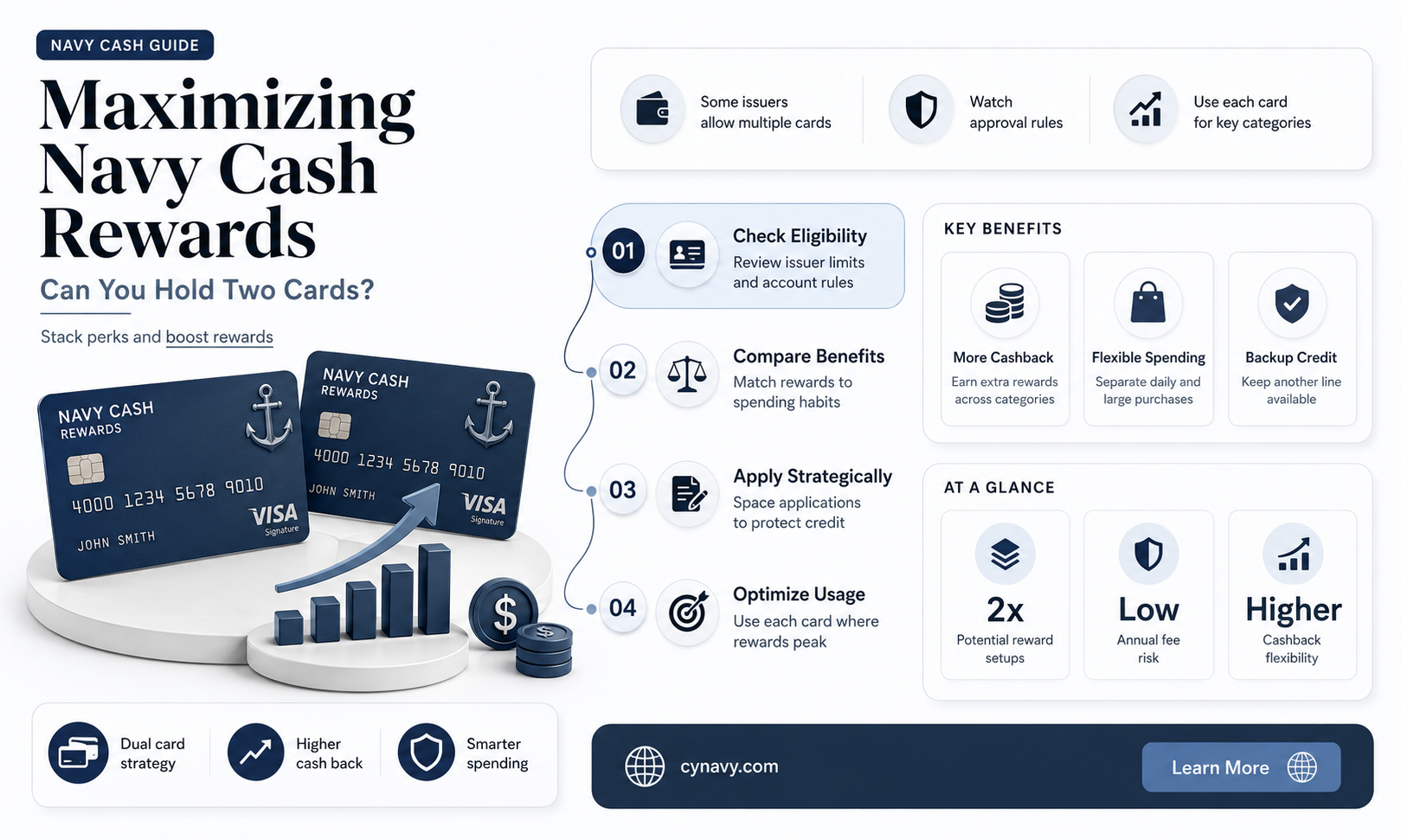

When considering maximizing cash back rewards, many individuals wonder if it’s possible to hold two cash rewards cards from Navy Federal Credit Union simultaneously. Navy Federal offers several cash back credit cards, each with unique benefits and categories, making it appealing to combine them for greater savings. However, the ability to hold multiple cash rewards cards from the same issuer depends on Navy Federal’s policies, including creditworthiness, account history, and their terms regarding multiple card ownership. While some financial institutions allow multiple cards, others may restrict it to prevent overextension or fraud. To determine eligibility, it’s essential to review Navy Federal’s specific guidelines or consult with a representative to understand if holding two cash rewards cards aligns with their rules and your financial goals.

Explore related products

What You'll Learn

![]()

Eligibility for Multiple Cards

Obtaining multiple cash rewards cards from Navy Federal Credit Union (NFCU) hinges on understanding their eligibility criteria and application policies. While NFCU doesn’t explicitly prohibit holding more than one rewards card, approval for a second card depends on factors like your credit history, income, and existing relationship with the credit union. Members with a strong credit profile, consistent repayment behavior, and a history of responsible account management are more likely to qualify for additional cards. However, NFCU may limit the number of cards you can hold simultaneously to mitigate risk and ensure financial stability.

To assess eligibility, NFCU evaluates your credit score, debt-to-income ratio, and overall financial health. A credit score of 700 or higher typically strengthens your case, though exceptions exist for long-standing members with proven loyalty. If you’ve held a Navy Federal card for at least six months and consistently meet payment deadlines, your chances improve. Conversely, recent applications for credit or high credit utilization may hinder approval. Practical tip: check your credit report for errors before applying, as inaccuracies can unfairly impact your eligibility.

Another critical factor is your income and employment status. NFCU requires sufficient income to support multiple credit lines, ensuring you can manage repayments without strain. If your income has increased since your last application, update your profile with NFCU to reflect this change. Self-employed individuals or those with variable income may need additional documentation, such as tax returns or bank statements, to demonstrate financial stability. Proactive communication with NFCU’s customer service can clarify specific requirements tailored to your situation.

Strategically spacing out applications is key to maximizing approval odds. Applying for two cards simultaneously often results in denial due to perceived risk. Instead, wait at least 90 days between applications, allowing time for your credit profile to stabilize. If denied, inquire about the reason and address the issue before reapplying. For instance, if high credit utilization was the cause, pay down balances to below 30% of your limit before attempting again. Patience and financial discipline are essential in this process.

Finally, consider the value of holding multiple cards versus the potential drawbacks. While diversifying rewards can be advantageous, managing multiple accounts requires vigilance to avoid missed payments or overspending. Evaluate whether the benefits—such as higher cash-back tiers or bonus categories—outweigh the administrative effort. If you’re confident in your ability to manage multiple cards responsibly, proceed with a clear plan to maximize rewards while maintaining financial health.

Can Army and Navy Athletes Secure NIL Deals? Exploring the Rules

You may want to see also

Explore related products

![]()

Credit Score Requirements

To qualify for multiple cash rewards cards from Navy Federal Credit Union, understanding the credit score requirements is crucial. Navy Federal typically looks for a good to excellent credit score, generally defined as 670 or higher. However, for premium rewards cards, such as those offering higher cash back rates or additional perks, a score of 740 or above is often preferred. This threshold ensures that applicants demonstrate a strong history of financial responsibility, reducing risk for the lender.

While credit score is a primary factor, Navy Federal also evaluates overall creditworthiness, including payment history, credit utilization, and length of credit history. For instance, even with a score above 700, a recent late payment or high debt-to-income ratio could hinder approval for a second card. Conversely, a score slightly below 700 but with a pristine payment record might still qualify, especially if you’re an existing member in good standing. This holistic approach means that meeting the minimum score is necessary but not always sufficient.

If you’re considering applying for a second cash rewards card, check your credit score beforehand using free tools like Credit Karma or AnnualCreditReport.com. Aim to address any discrepancies or negative marks on your report, as these can impact approval odds. Additionally, space out applications by at least six months to minimize the impact of hard inquiries on your credit score. Navy Federal may be more lenient with existing members, but multiple recent inquiries could raise red flags.

A practical tip for improving your chances is to diversify your credit portfolio before applying. For example, if you already have a Navy Federal credit card, consider adding a loan or savings account with them to strengthen your relationship. This demonstrates loyalty and financial stability, which can offset marginal credit score differences. Remember, Navy Federal prioritizes members’ financial health, so aligning with their values can work in your favor.

Finally, if your credit score falls short, focus on building it before applying. Pay bills on time, keep credit utilization below 30%, and avoid opening new accounts unnecessarily. For those with scores in the 670–700 range, start with a basic cash rewards card and use it responsibly for 6–12 months. This establishes a positive payment history with Navy Federal, increasing the likelihood of approval for a second card later. Patience and strategic financial management are key to navigating credit score requirements effectively.

Can Navy Veterans Receive Social Security Benefits? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Application Process Details

Applying for multiple cash rewards cards from Navy Federal Credit Union requires a strategic approach, as the institution evaluates each application based on individual creditworthiness and existing account relationships. Start by reviewing your credit report to ensure accuracy and identify areas for improvement, as a higher credit score increases approval odds. Navy Federal typically prefers members with a solid history of responsible credit use and stable income. If you already hold one cash rewards card, assess your account standing—consistent on-time payments and low credit utilization are essential.

The application process itself is straightforward but demands careful timing. Navy Federal may impose a waiting period between applications, often six months or more, to prevent overextension. To maximize approval chances, space out applications and avoid applying for other credit products simultaneously. When completing the online form, provide precise financial details, including annual income and employment status. If you’re an existing member, ensure your account is in good standing, as this can expedite approval.

One critical factor is Navy Federal’s policy on multiple cards. While they allow members to hold more than one credit card, approval for a second cash rewards card isn’t guaranteed. The credit union evaluates your overall credit limit across accounts, so if your existing limit is high, they may deny the second card. To mitigate this, consider requesting a lower credit limit on the new card or paying down balances on existing cards before applying.

A practical tip is to call Navy Federal’s customer service before applying. Representatives can provide insights into your eligibility and suggest steps to improve your chances. For instance, they might recommend waiting until your credit score rises or reducing outstanding debt. Additionally, leverage your membership benefits—longer membership tenure and active account usage can work in your favor. Finally, monitor your application status closely; if denied, wait at least six months before reapplying to avoid damaging your credit score further.

Navy Federal Car Insurance: Coverage Options and Benefits Explained

You may want to see also

Explore related products

![]()

Rewards Program Benefits

Navy Federal Credit Union offers a range of cash rewards cards, each with its own set of benefits tailored to different spending habits and financial goals. One common question among members is whether it’s possible—or advantageous—to hold two cash rewards cards simultaneously. The short answer is yes, but the real value lies in understanding how to maximize the rewards program benefits across multiple cards. Here’s how to approach this strategically.

First, analyze the rewards structure of each card. Navy Federal’s cash rewards cards often feature tiered earning rates, such as 1.5% on all purchases or higher rates in specific categories like gas, groceries, or dining. Holding two cards allows you to double-dip by using one card for everyday spending and the other for category-specific bonuses. For example, pair the Navy Federal More Rewards American Express Card, which offers 3x points on travel and dining, with the Navy Federal Cash Rewards Visa Card for its flat 1.75% cashback on all purchases. This combination ensures you’re earning the highest possible rewards across all spending categories.

However, managing two cards requires discipline to avoid overspending or missing payments. Set clear guidelines for each card’s use—for instance, use the Amex card exclusively for travel and dining, while the Visa handles all other transactions. Additionally, monitor your credit utilization ratio, as opening multiple cards can temporarily lower your credit score. Aim to keep your total credit utilization below 30% to maintain a healthy credit profile.

Another benefit of holding two cash rewards cards is the potential to earn sign-up bonuses twice. Navy Federal often offers introductory bonuses, such as $200 cashback after spending $3,000 in the first 90 days. By strategically timing your applications, you can meet the spending requirements for both cards and pocket two bonuses. Just ensure the combined spending aligns with your budget to avoid unnecessary debt.

Finally, consider the long-term value of holding two cards. While the rewards can be lucrative, evaluate the annual fees (if any) and whether the cashback earned outweighs the costs. Navy Federal’s cards often waive fees for military members, making this strategy more accessible. Regularly review your rewards earnings and adjust your card usage to ensure you’re maximizing benefits without unnecessary complexity. With careful planning, holding two cash rewards cards from Navy Federal can significantly boost your cashback earnings.

Are DC Residents Receiving Mysterious Calls from Navy Yard?

You may want to see also

Explore related products

![]()

Annual Fee Considerations

Annual fees can significantly impact the value of holding multiple cash rewards cards from Navy Federal Credit Union. While some cards waive annual fees entirely, others may charge upwards of $49 to $195 annually. Before applying for a second card, calculate the breakeven point: divide the annual fee by the cash back rate to determine how much spending is required to offset the cost. For instance, a card with a $95 annual fee and 1.5% cash back requires $6,333 in annual spending to justify the fee. If your total spending across both cards doesn’t meet this threshold, the fee could negate the rewards earned.

Consider the combined value of benefits offered by each card when evaluating annual fees. Some Navy Federal cards include perks like rental car insurance, travel credits, or statement credits that can offset the fee. For example, if a card offers a $100 annual travel credit and charges a $95 annual fee, the net cost is effectively $5. If both cards you’re considering offer overlapping benefits, the second card’s fee may not be worth it unless the rewards structure significantly outperforms the first.

Timing plays a critical role in minimizing annual fee impact. Navy Federal occasionally offers promotional periods with waived fees for the first year, providing a trial period to assess the card’s value. If you’re considering a second card, apply during such promotions to avoid immediate costs. Additionally, monitor your spending patterns throughout the year; if the second card isn’t delivering sufficient value, downgrade or close it before the next annual fee posts to avoid unnecessary charges.

For households with shared finances, coordinating card usage can maximize rewards while managing fees. If one partner holds a card with an annual fee, ensure their spending aligns with the card’s highest reward categories to offset the cost. A second card might be justified if it fills a gap in rewards, such as offering higher cash back on groceries or gas. However, avoid duplicating rewards structures, as this dilutes the overall return on investment and increases fee burden without proportional benefits.

Finally, leverage Navy Federal’s customer service to negotiate annual fees, especially if you’re a long-standing member with a strong credit history. Some issuers waive or reduce fees for loyal customers who threaten to close an account. Before committing to a second card, inquire about fee waivers or retention offers. This proactive approach can preserve your rewards earnings while maintaining access to multiple cards. Always weigh the long-term value against the recurring cost to ensure financial efficiency.

How to Get Navy Federal to Release Your Pending Deposit Early

You may want to see also

Frequently asked questions

Navy Federal Credit Union typically allows members to hold only one Cash Rewards card at a time. Applying for two simultaneously may result in denial or account review.

Navy Federal generally restricts members to one Cash Rewards card per individual, regardless of account type. Business and personal cards are still subject to this limitation.

Closing and reopening a Cash Rewards card may not be approved, as Navy Federal evaluates eligibility based on your overall relationship and credit history.

Yes, spouses can each have their own Navy Federal Cash Rewards card, provided they meet individual eligibility requirements and are separate primary account holders.

Navy Federal typically does not allow members to hold two Cash Rewards cards simultaneously, even if one is an upgrade. The existing card may need to be closed first.